Blog

Pay by Bank in action: how to build a high-performing Pay by Bank checkout experience

The ultimate guide to designing a Pay by Bank experience that customers actively choose time and time again.

Read more

)

Featured articles

)

7 Jan 2026

Recurring payments

What does 2026 hold for VRP?

Find out why VRP (AKA Bank on file) is set for a new wave of use cases in 2026.

)

10 Oct 2025

Payments

The complete guide to Pay by Bank: what is it and how does it work?

The complete guide to Pay by Bank, the fast-growing online payment method, offering an alternative to cards. Should your business be offering it at checkout?

)

22 Oct 2025

Ecommerce

Everything you need to know about the TrueLayer Network in 90 seconds

Find out how the TrueLayer Network is changing Pay by Bank from a simple checkout option into a conversion engine.

Viewing:

)

6 Aug 2026

Payments

Pay by Bank: the iDEAL opportunity for payments in the Netherlands

iDEAL is disappearing and migrating to Wero isn't the only option. See how Pay by Bank could be the answer in the Netherlands.

)

14 Jul 2026

Payments

Payment choice, not cards by default: the policy view on agentic payments

How do the payments industry and policymakers ensure agentic payments aren’t card-native by default, and who is responsible for driving that agenda?

)

10 Jul 2026

Payments

Ireland's moment: why the EU Presidency matters for the future of payments

13 years on from Ireland's previous EU Council Presidency, what's changed and what needs to be done next?

)

6 Jul 2026

iGaming

Affordability checks are mandatory. How you run them is your choice

Affordability checks are mandatory. How can you build high-converting affordability checks directly into your payments infrastructure?

)

25 Jun 2026

Payments

Red Card: How a card outage put England's merchants on the sideline

Card payments failed across the UK at half-time of England's World Cup match. Two venues kept trading. Pay by Bank ran on different rails.

)

5 Jun 2026

Products

Pay by Bank - Credit: our latest step towards a complete Pay by Bank payments network

Truelayer CEO, Fra, on our latest step towards a complete Pay by Bank payments network

)

27 May 2026

Recurring payments

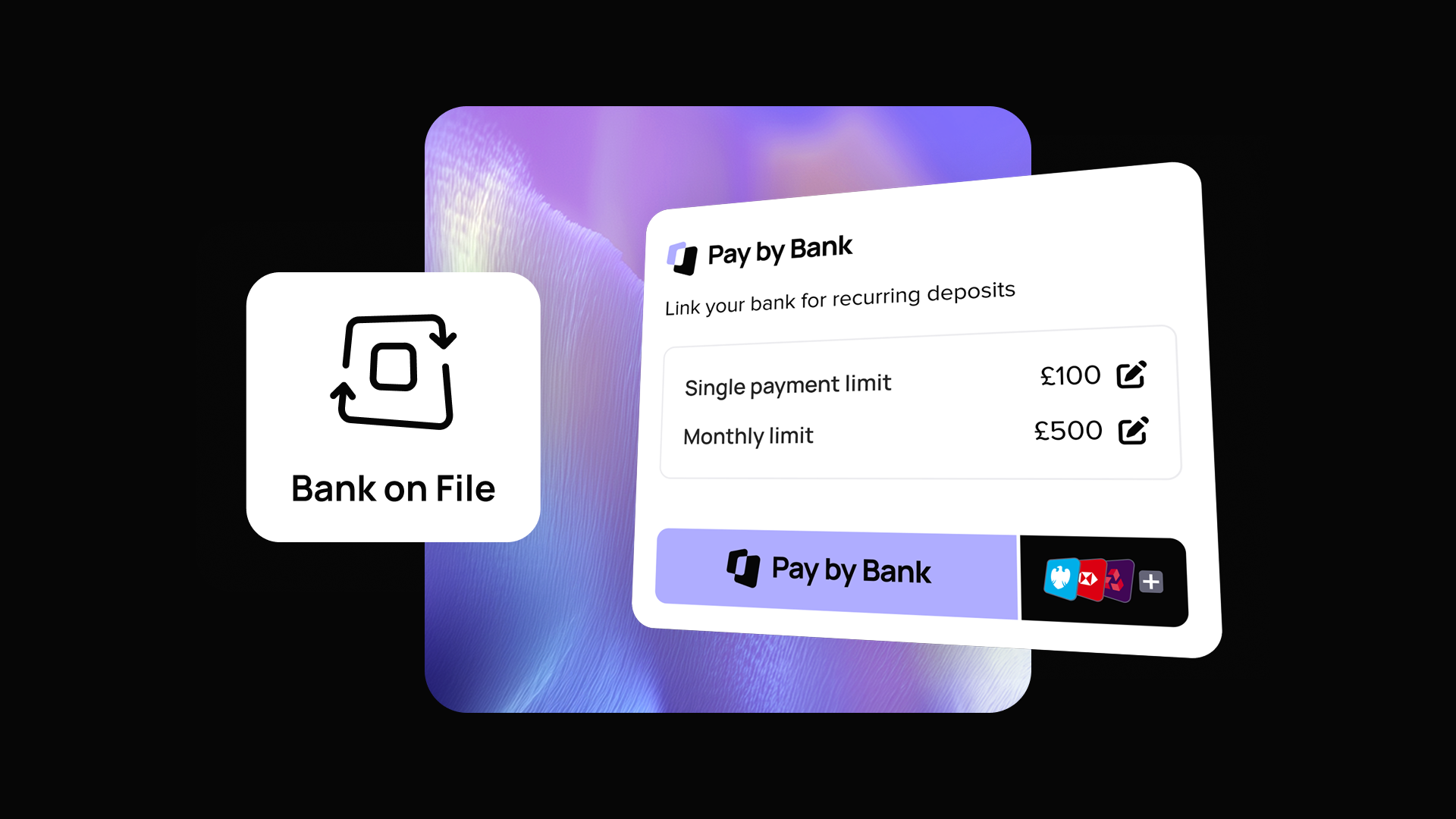

Bank on File: this is only the start

Bank on File further moves online commerce towards payment systems that are faster, more efficient, and built for the internet economy.

)

14 May 2026

Recurring payments

The complete guide to Bank on File: from one-click checkouts to streamlined subscription payments

The complete guide to Bank on File, the next generation of one-click and recurring payments. What is it, and how does it work?

)

13 May 2026

Products

Behind the build: how we made Bank on File a bit more human

Bank on File is about to transform recurring payments and one-click checkouts. Here's how me built it for merchants and consumers alike.

)

12 May 2026

Recurring payments

From principle to practice: Why UKPI is the crucial test-bed for open finance

Rob Kerrigan explains why the UK Payment Initiation (UKPI) framework is the crucial test-bed for the future of open finance, bridging the gap from principle.

)

4 May 2026

Recurring payments

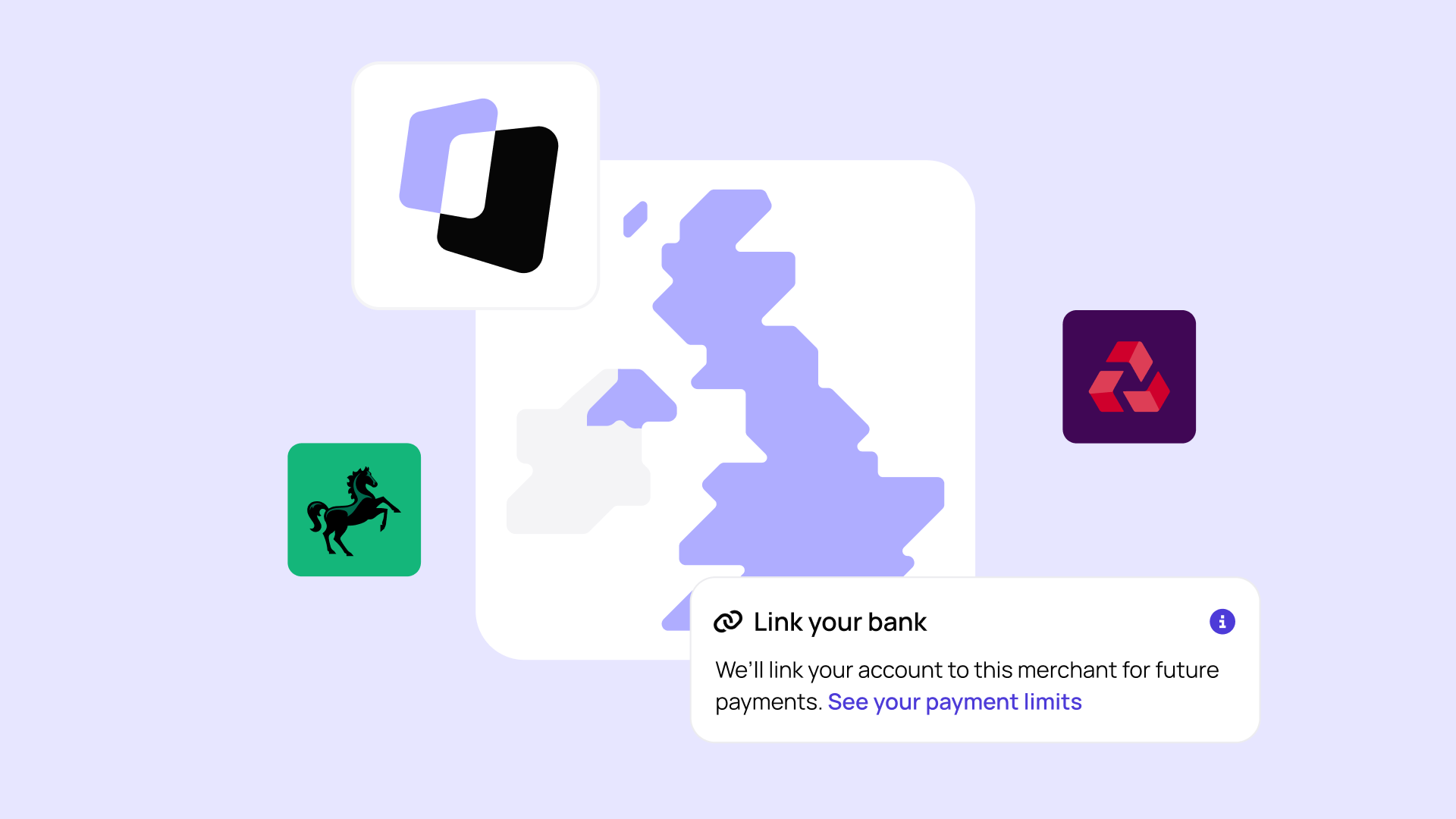

Everything you need to know about Bank on File

What is Bank on File and how does it work? What are the benefits for merchants and for consumers? And how does it compare to card on file and direct debit?

)

26 Mar 2026

Recurring payments

Bank on File is on the launch pad

Bank on File is launching to bring recurring payments (VRP) to Pay by Bank. Get faster settlement, lower costs, and secure, consumer-controlled subscriptions.

Browse by category

Get started

Talk to us

Curious about where our open banking payments network could take your business?

Keep exploring