Bank on File: this is only the start

)

)

This article was originally delivered as a keynote, by TrueLayer CEO and Co-Founder Francesco Simonsechi at our recent event, "Building for the next era of payments".

For decades, ecommerce has relied on cards. But the 16-digit number your card is based on is older than the internet. Think about that. We have built the entire digital economy on top of an idea, on top of infrastructure, which was never designed for it.

The card schemes have done a reasonable job of adapting cards for the internet. But each adaptation added another layer. A layer of complexity. A layer of cost. Another intermediary. Sometimes all three.

And because merchants had to accept card payments, they had to accept everything that came with them. The middlemen, the rising fees, the friendly fraud and the unilateral chargebacks.

Finding the exit ramp of the card-on-file spaghetti junction

The result is a complex patchwork of add-ons, something that looks like a spaghetti junction. Every new requirement added another ramp, another toll, another loop.

Today, every online card transaction touches five or six different intermediaries: wallets, tokenisation, card updaters, click-to-pay, risk tools. The list goes on. Each one takes a cut. Each one adds complexity. Each one adds a point of failure.

“If card payments are like a spaghetti junction, then Pay by Bank, on the other hand, is more like a bullet train — point A to point B, quickly and reliably.

Francesco Simoneschi, CEO and Co-founder

I'm Italian — so I'll put it this way. If every time I ordered a pizza, five or six people took a slice before it reached me, I'd be furious. That's the card system. And merchants have been living with it for decades.

And if card payments are like a spaghetti junction, then Pay by Bank, on the other hand, is more like a bullet train — point A to point B, quickly and reliably.

At TrueLayer, we know that the next era of payments is Pay by Bank. It's instant. It's bank-based. It's lower cost. It's more secure. It has all the right ingredients for digital commerce, without the long list of intermediaries the card system accumulated over seventy-five years adding any unnecessary forks in the track.

Pay by Bank has already proved its value for one-off payments. Summer is almost here — and today, you can book a Ryanair flight with Pay by Bank, buy sunglasses on eBay, pay for your sunscreen on Amazon, top up your Revolut when you land, and order lunch by the pool on Just Eat. All using Pay by Bank. The infrastructure is real, and merchants are already using it.

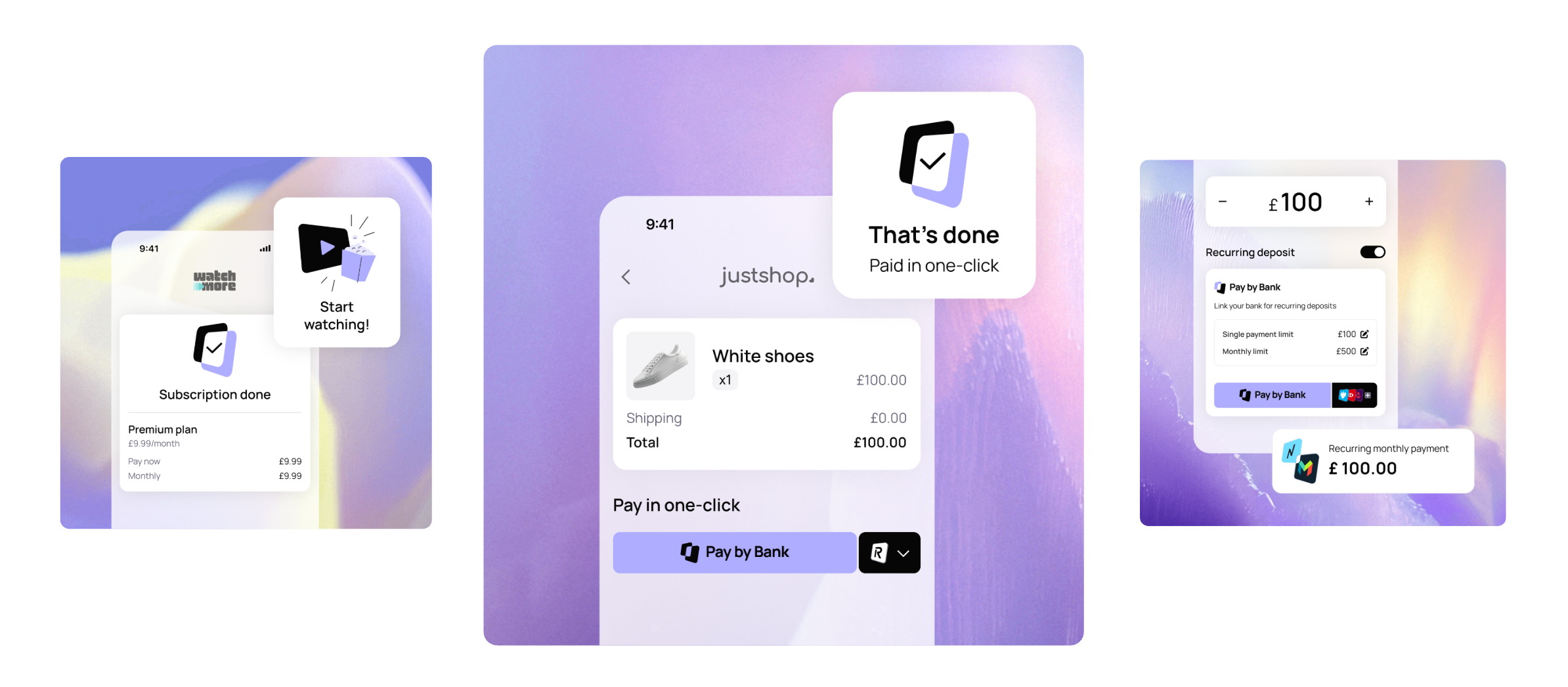

But until today, Pay by Bank had one major limitation: it couldn’t be saved for merchant-initiated payments like subscriptions, memberships, or one-click checkout. Merchant-initiated payments — the repeat, recurring transactions that make modern commerce run. These remained the domain of card payments.

Today, that changes. It changes with something we call Bank on File.

Why Bank on File isn’t a step forward, but a leap

Bank on File unlocks the full power and potential of Pay by Bank.

Bank on File works everywhere card on file does. Subscriptions of every kind — your Spotify, Netflix, ChatGPT, gym membership, school fees. Regular purchases like your weekly Tesco shop. And there’s utility bills, phone contracts, food delivery apps, and ride-sharing. It can even be used for one click checkouts

Bank on File does all of this faster, cheaper, and more securely.

)

And here's what makes it genuinely different: it doesn't store card details. It stores the user’s consent. Programmable consent is the core idea of Bank on File — and its superpower. Unlike a card, the mandate won’t expire when the card does. It fixes the graveyard of expired, lost and stolen cards that merchants manage today, all while giving consumers cleaner control over what they've authorised.

This is a major step forward

I want to be clear: today isn't about a TrueLayer product. It's about a bigger shift — to instant, account to account payments that can be reused.

Transitioning payments from diesel to electric

We are going from old to new, upgrading the payment grid from diesel to electric.

This transition is already happening across the world. PIX in Brazil. UPI in India. Swish in Sweden. Regulators, banks, merchants and consumers everywhere are moving in the same direction: towards payment systems that are faster, more efficient, and built for the internet economy.

With Bank on File, the UK also takes a significant step in that direction.

TrueLayer’s role in this is to turn that infrastructure into a network that merchants and consumers can actually use.

But we also need to thank all the teams and external partners who made this possible. Years of infrastructure work, regulatory engagement, bank-by-bank progress, product thinking, and close collaboration with our merchants.

And this is only the start.

Together, we’re charting a path to a world where Pay by Bank isn't an alternative payment method — it's the default one. A complete payment network, built for modern commerce.

Cards have had a seventy-five year head start on us.

Bank on File starts today.

)

TrueLayer part of FCA's Supercharged Sandbox to test agentic payments

)

Payment choice, not cards by default: the view on agentic payments

)