The complete guide to Bank on File: from one-click checkouts to streamlined subscription payments

)

)

Pay by Bank, the payment method that lets customers pay for things directly from their bank account, without the need for card networks, is now on the checkouts of some of the world’s biggest ecommerce retailers — including Amazon, eBay and Just Eat.

Until now, Pay by Bank has been primarily used for single, one-off payments. For the consumer, standard Pay by Bank payments require a few easy steps, and they don’t need to type in any lengthy card details. But for things like one-click checkouts and recurring payments (like subscriptions and instalments), the experience needs to be even smoother and faster, and sometimes completely invisible to your users.

That’s where Bank on File comes in.

In summary

Bank on File is a new capability of Pay by Bank that lets merchants capture user consent, so you create an instant one-click payment experience or take repeat payments into the future.

Bank on File can be used for things like creating one-click checkout experiences, collecting subscription payments, and for utilities and billing.

Bank on File can help remove friction from repeat purchases, increasing conversion rates, and features like confirmation of funds (that show whether a consumer has sufficient funds in their account before an attempted payment) reduces the chance of a payment failing.

What is Bank on File?

Bank on File is a new capability of Pay by Bank that lets merchants capture user consent, so you create an instant one-click payment experience or take repeat payments into the future. This could be for fixed or variable amounts, at regular or irregular intervals.

This means that, instead of your customer having to use the standard Pay by Bank journey each time they want to make a payment, they instead start by authorising you, as the merchant, to collect payments from them by securely linking their bank account for future payments.

When that customer buys something from you next time, they can do so in just one click, or — if they’re paying for something as a subscription or via instalments, it can happen without them needing to do anything at all.

You can put parameters in place, which essentially mean limits on how often or the amount you can pull payments from the user’s account, so they feel fully in control of their spending. Consumers can also cancel these at any time.

How is Bank on File different to VRP?

You may already have heard of something called variable recurring payments (VRP). VRP is an open banking-powered payment instruction that allows providers to initiate payments of varying amounts from a user’s bank account with agreed-upon limits.

So far, so similar to Bank on File.

The difference between Bank on File and VRP, is that Bank on File is the experience you’re offering, while VRP is simply one framework that can enable that Bank on File experience.

For example, payment methods like Direct Debit may have limitations when used on its own, but when combined with Pay by Bank, VRP and other account to account payment methods, it can result in the best possible recurring payment experience.

and other account to account payment methods can also be used as part of the underlying payment rails that power the best Bank on File experience.

VRP is also still being developed, with certain use cases now possible such as sweeping, which means payments between two accounts belonging to the same person. Sweeping VRPs are good for credit card repayments, smart savings and overdraft management.

Commercial VRPs (sometimes referred to as cVRPs) are for payments between two different parties, typically a consumer and a business. The first launch of cVRP, called Wave 1, scheduled for late May 2026, will mean VRP can be used for things like utility bills and train tickets. Wave 2, which is everything else, is under development.

Regardless of the underlying payment method, TrueLayer provides Bank on File as part of a single API integration, meaning you’re always getting the best possible experience.

How does Bank on File work?

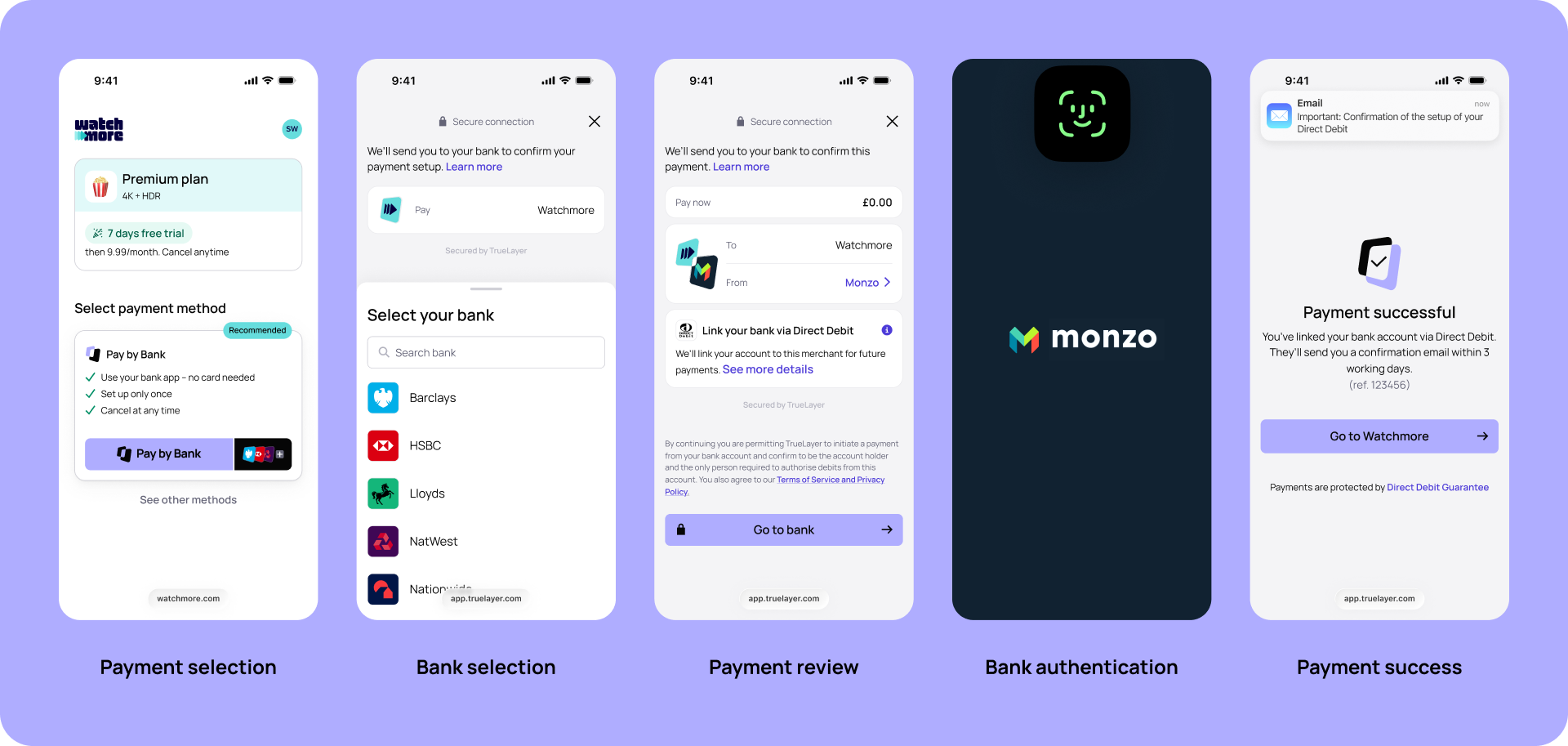

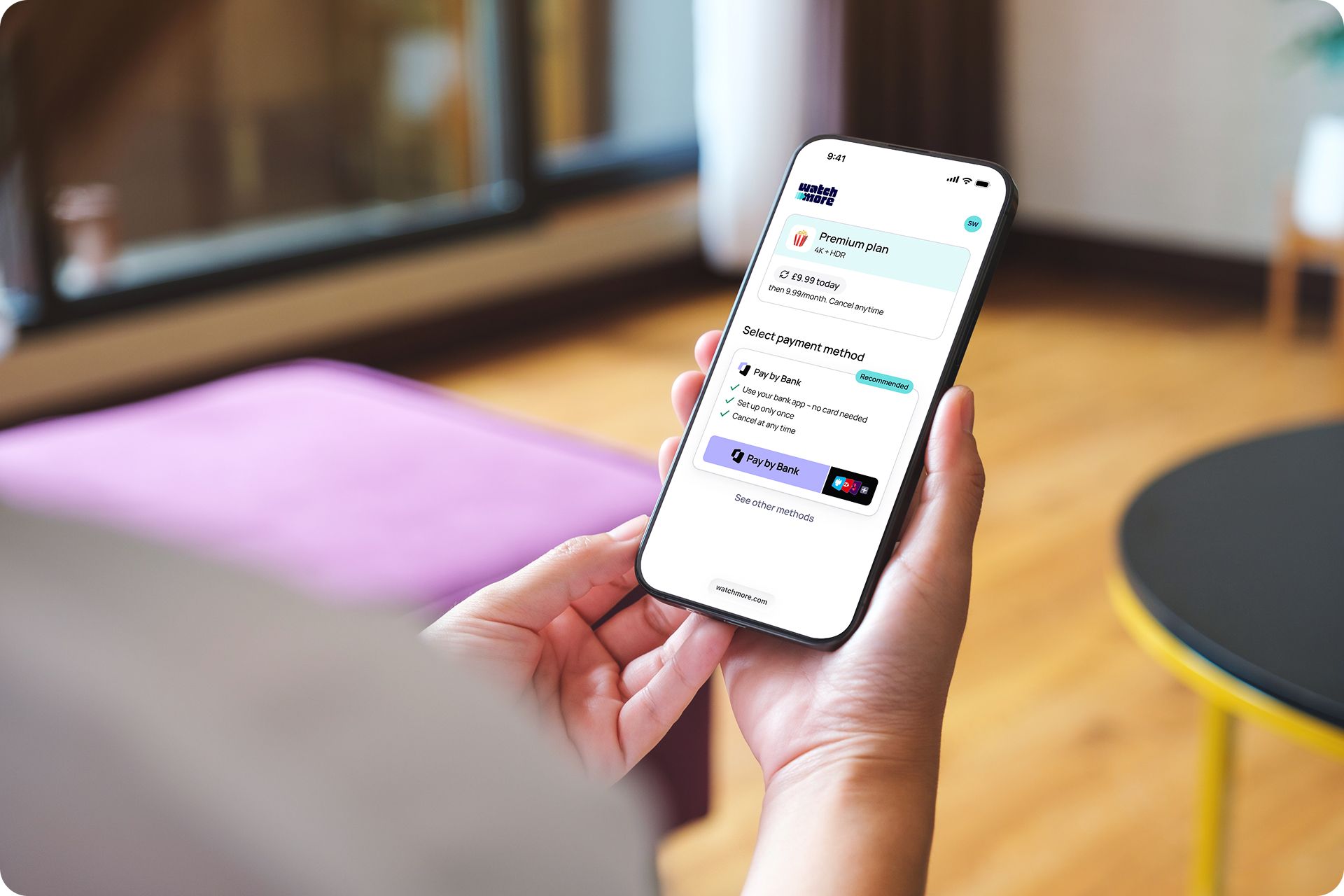

For the consumer, Bank on File looks a lot like Pay by Bank when they make their first payment and/or link their bank account for future payments.

At checkout, you select Pay by Bank (Simple language like Link your bank will explain how this particular payment method works)

You select your bank from the list available

You are then sent to your bank account to securely authenticate the payment set up (where the exact parameters of future payments are clearly stated)

You’re then sent back to the merchant, where your completed payment and bank linking is confirmed instantly.

)

For any future payments, the process is even quicker. For one-click, simply select Pay by Bank at checkout, and click ‘Pay with [Bank]’. For subscription payments, where the payment is collected every month, the consumer doesn’t need to do anything, with the payment automatically happening as part of the pre-agreed timeframe as set out in the initial set up.

What can you use Bank on File for?

Bank on File can theoretically be used for any kind of repeat or recurring payment, but there are a few use cases where it is particularly useful:

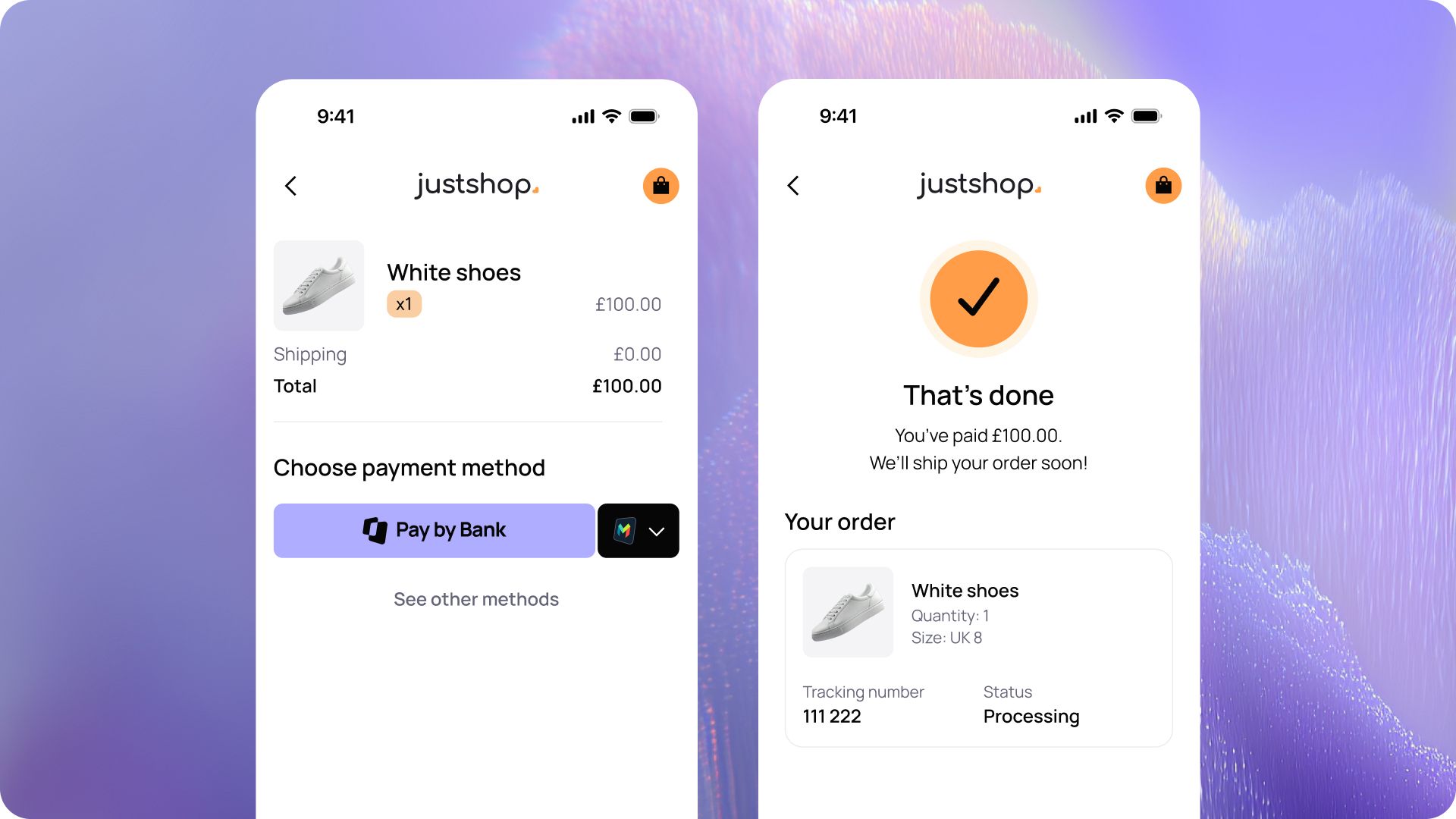

One-click checkout

For any use cases where your customers buy from you on a regular basis, such as takeaways and high-frequency online shopping, one-click checkouts remove any friction that stops your shoppers from making their purchases. One-click checkouts powered by Bank on File give your shoppers the simplest and quickest way to pay whenever they shop with you.

)

Subscription and membership payments

Bank on File is perfect when you need to collect payments on a consistent basis, be it weekly, monthly or annually. Bank on File allows you to create long-lasting mandates that won’t expire, unlike card payments, reducing involuntary churn.

Utility and billing

Bank on File can also be used to pay utility bills, whether that’s for fixed or variable amounts. It can also be used for one-off or ad-hoc payments if, for example, a consumer’s regular payment hasn’t covered all of their costs. This flexibility can help reduce defaults and increase collection success rates.

Instalment payments

For use cases where consumers pay for a single high-value purchase over a set period of time with a defined end date. By offering this way to pay, merchants can increase conversion for high-ticket items.

A combination of several use cases

Bank on File has the added advantage of being an option if you need more than one of these use cases, for example if your customers pay a monthly subscription for access to a specific service, but sometimes also buys a product on an ad-hoc basis. With Bank on File, this can all be handled through a single mandate.

What are the benefits of using Bank on File?

In addition to the benefits of using single-payment Pay by Bank, like lower operational costs, fully secure payments for merchants and consumers, instant refunds and reducing reliance on card payments, Bank on File has some unique advantages:

)

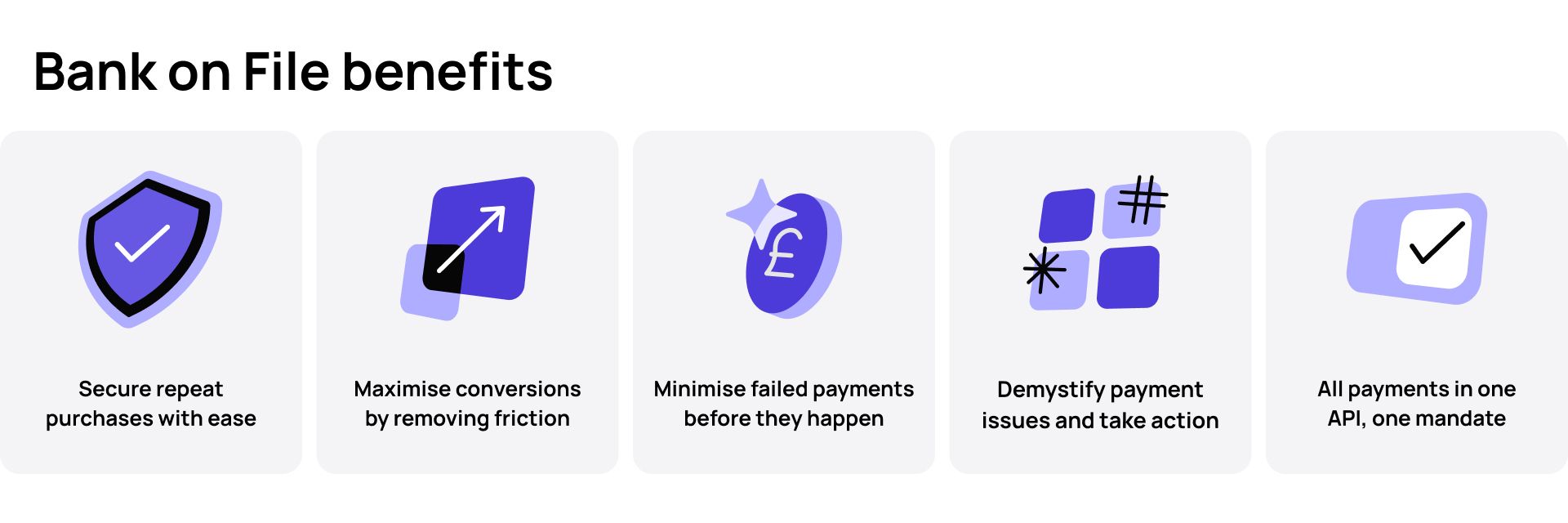

Secure repeat purchases with ease: Bank on File securely tokenises customer bank account information to allow merchants to collect future payments without any unneeded friction, as long as the mandate is active.

Maximise conversions by removing friction: Create genuine one-click payment experiences, reducing cart abandonment and increasing conversion and repeat purchases.

Minimise failed payments before they ever happen: Bank on File includes a feature called confirmation of funds that allows merchants to silently check whether a customer has sufficient funds to make an upcoming payment. You can then react accordingly if they don’t, communicating with the customer or reducing the amount of the upcoming payment.

Demystify payment issues and take action: alongside confirmation of funds, get other information on reasons for failed payments and other issues so you can recover revenue even faster. Plus, there are no retry fees, so you can attempt another payment without incurring additional costs.

All repeat and recurring payments in one API as part of one mandate: From subscriptions to instalments, manage every recurring payment scenario effortlessly as part of one API if you work with TrueLayer to offer Bank on File at checkout.

How does Bank on File compare to other payment methods?

Merchants typically have two options if they want to collect recurring payments and/or create a one-click checkout: card on file and traditional Direct Debit.

Here’s how those payment methods stack up when it comes to recurring payments:

Card-on-file payments

A card-on-file transaction (also known as a continuous payment authority) is a transaction where a cardholder authorises a merchant to store their payment details, and then also authorises that same merchant to bill the stored account for recurring payments.

While card-on-file has well-established consumer protections, any card turnover from card expiry or loss will render the mandate useless. Consumers also have little visibility or control over the mandate, meaning they can fall victim to subscription traps by unscrupulous merchants.

For merchants, card on file means the same high card fees as you would have with ad-hoc payments, along with potential settlement times of up to three days. Chargebacks are also a challenge with card on file payments. They’re difficult to manage or appeal, and there’s no time limit for consumers to request them.

Traditional Direct Debit

Direct Debit is an instruction from your customers to their bank or building society. It allows a consumer to authorises the merchant they want to pay to collect varying amounts from their account — but only if they’ve been given advance notice of the amounts and dates of collection.

Direct Debit comes with the Direct Debit guarantee, meaning consumers are protected if businesses act within defiance of the mandate. On the flipside, the set up experience is often prone to human error — with users manually typing (or mistyping) several pieces of information. And visibility of active mandates is poor, with consumers often struggling to amend or cancel mandates.

For merchants, they can avoid the costly fees of card payments when using Direct Debit, but — again — slow settlement causes cash flow issues, and unfortunately makes Direct Debit unusable for merchants who need the first payment to take place in real-time.

Recurring payment methods compared

| Card on file | Traditional Direct Debit | Bank on File | |

|---|---|---|---|

| Setup speed | ✅ Fast | ❌ Slow (up to 10 days) | ✅ Fast |

| Settlement speed | ❌ Slow (usually 1–3 business days) | ❌ Slow (3 days in most cases) | ✅ Fast |

| Simplicity | ❌ "Hold on… where’s my wallet?" | ❌ Limited | ✅ App2app |

| Consumer control & visibility | ❌ Low. Consumers prone to subscription traps and unexpected charges | ❌ Low. No flexibility to adapt Direct Debit mandate | ✅ High |

| Price | ❌ Expensive | ✅ Cheap | ✅ Competitive |

| Lifespan | ❌ Limited | ✅ Perpetual | ✅ Perpetual (subject to consumer control) |

| Security | ❌ Weak (high fraud) | ✅ Strong | ✅ Strong (Bank on File requires SCA to set-up) |

Will consumers use Bank on File?

Any payment method needs the consumer to trust and choose it when they see it at checkout. To consumers, Bank on File has the same payment experience as Pay by Bank, which already sees over 37 million UK payments every single month, and 6 million of those are already VRP payments — which as mentioned earlier, are a key framework for Bank on File payments. So, to put it simply, there is good reason to think that consumers will happily use Bank on File.

There are also specific consumer benefits of Bank on File. It settles immediately, unlike Direct Debit, with which payments run on three-day cycles and can take up to three days to settle. Consumers know what they’ve paid.

And the flexibility built into Bank on file gives consumers more certainty of what will leave their account when, which also means fewer failed or bounced payments for merchants.

At a time when 7.4 million consumers feel burdened by bills and credit commitments, and 5.5 million have missed payments in the last six months, Bank on File offers a better alternative to what consumers normally have to pay with.

Is Bank on File safe?

In short, yes. Bank on File is a capability of Pay by Bank, which is a safe and secure payment method.

Bank on File is significantly more secure than card on file. Bank on File doesn’t store raw bank account details. After the initial bank-level authentication, we securely tokenise the details, meaning we use a non-sensitive placeholder to facilitate future payments.

This approach, combined with strong customer authentication at setup, drastically reduces the risk of fraud compared to vulnerable card-not-present transactions.

And when Pay by Bank providers like TrueLayer enable payments for a merchant or other business, they enter into a commercial contract with that business and undertake due diligence on the business as part of that. This reduces the likelihood that bad actor merchants would use open banking to commit fraud.

Bank on File with TrueLayer

TrueLayer’s Bank on File means all of your recurring payments in one simple API, meaning just one integration that’s always improving to provide you with the most effective payment technology available.

)

Working with TrueLayer also gives you access to the fastest-growing Pay by Bank network in Europe, with over 20 million consumers in the network, accounting for 47% of all UK Pay by Bank transactions. With higher volumes of customer data, we ensure your user journeys are brilliantly optimised, turning every shopper into a loyal customer.

To find out more about how Bank on File could help revolutionise your recurring payments, speak to one of our Pay by Bank experts.

)

TrueLayer part of FCA's Supercharged Sandbox to test agentic payments

)

Payment choice, not cards by default: the view on agentic payments

)