)

)

Europe’s open banking ecosystem might get a major boost. Last month, the EU Commission published a long-awaited proposal aimed at increasing instant payments coverage throughout Europe. It seeks to make instant payments available, affordable and secure for European consumers.

That’s big news because instant payments coverage is key to the success of open banking. Compared to other methods, open banking can improve customer experience and deliver cost savings for businesses. But it’s difficult to achieve those benefits without making instant payment infrastructure widely available.

The EU Commission’s proposal looks to do just that. Despite these improvements, questions remain around charges, verification and cross-border payments.

So what exactly is the Commission proposing? This article will give you the key points and look at a few missing pieces.

1. Banks must offer instant payments if they offer regular credit transfers

Euro transfers revolve around SEPA, the Single Euro Payments Area. Underpinned by a Regulation, SEPA is a European initiative that aims to harmonise cross-border and domestic cashless payments. Within SEPA, there are two schemes which banks and payment providers can use to make euro transfers between accounts — SEPA Credit and SEPA Instant.

The Commission’s proposal will require banks that offer SEPA Credit to also offer its counterpart, SEPA Instant. This provision is the backbone of the proposal and will go a long way towards making instant payments ubiquitous in Europe.

So why is that? Today, most account-to-account transfers in euros use SEPA Credit. It’s Europe’s default version of credit transfers, and it takes two to three days to settle.

Introduced in 2017, SEPA Instant was meant to enable faster and easier cross-border payments by giving customers a way to transfer money in real time.

But SEPA Instant is optional — EU banks don’t have to provide it, and little more than half do. Even though it’s been around for over five years, adoption has been slow. In some countries, virtually no one is able to take advantage of instant payments, with coverage as low as 4% in Denmark or 6% in Ireland.

The EU Commission’s proposal addresses this by requiring all banks that offer regular credit transfers to offer instant transfers too. This means that SEPA Instant will become much more widespread: the infrastructure will be there so that a majority of Europeans will be able to make instant payments.

)

2. Banks can’t charge more for instant payments

Adoption of instant payments is highest where charges are lowest or don’t exist at all.

Right now, some banks still charge for the use of SEPA Instant, which can be several euros for each transaction. This is a barrier to wider adoption, as customers can instead opt for a payment method they aren’t charged for, like cards. At the same time, many banks that offer SEPA Instant do so at no cost to the user, showing that free-to-payer is a feasible model.

)

Under the proposal, banks won’t be able to charge more for SEPA Instant transfers than they do for regular credit transfers. Since the majority of banks don’t charge their customers for using SEPA Credit, most SEPA Instant transfers would also carry no charge. Instant payments would finally become free for a very large number of Europeans.

There is, of course, the risk that charges for SEPA Credit will go up so banks can continue charging for SEPA Instant. This would undermine the adoption of instant payments and make the current legislative proposal much less effective.

The European Parliament and Council should consider this risk and take steps to ensure that charges for SEPA Credit do not increase artificially. Both SEPA Credit and SEPA Instant should be widely available to a majority of consumers — ideally at no cost.

3. More stringent verification measures to prevent fraud

The EU Commission’s proposal also adds protections against fraud by requiring the payment provider to check for mismatches between the name and IBAN of a payee.

Fraudsters sometimes pose as a legitimate payee to trick a business or consumer into sending a payment. In recent years, banks have tried to stamp out this type of fraud by requiring the matching of details like the payee’s name and IBAN with the information on file, before the payment is carried out. The proposal would make these steps mandatory.

However, name and IBAN verification must be implemented carefully so it doesn’t introduce unnecessary obstacles to completing payments. This is crucial with open banking payments. While name and IBAN verification can be relevant for some open banking use cases like peer-to-peer payments, it can also add friction to payment flows.

For example, when a business receives an open banking payment, the risks that this verification seeks to address are already mitigated. That's because the open banking provider has an established relationship with the business and pre-populates the payment details, ensuring the payment goes to the right place.

It’s important that the EU adopts a targeted, risk-based approach. Applying it to all use cases could create unnecessary friction that dissuades consumers from using open banking. There needs to be a carve-out in verification requirements for the open banking use cases described, where payee details are pre-populated by the open banking provider.

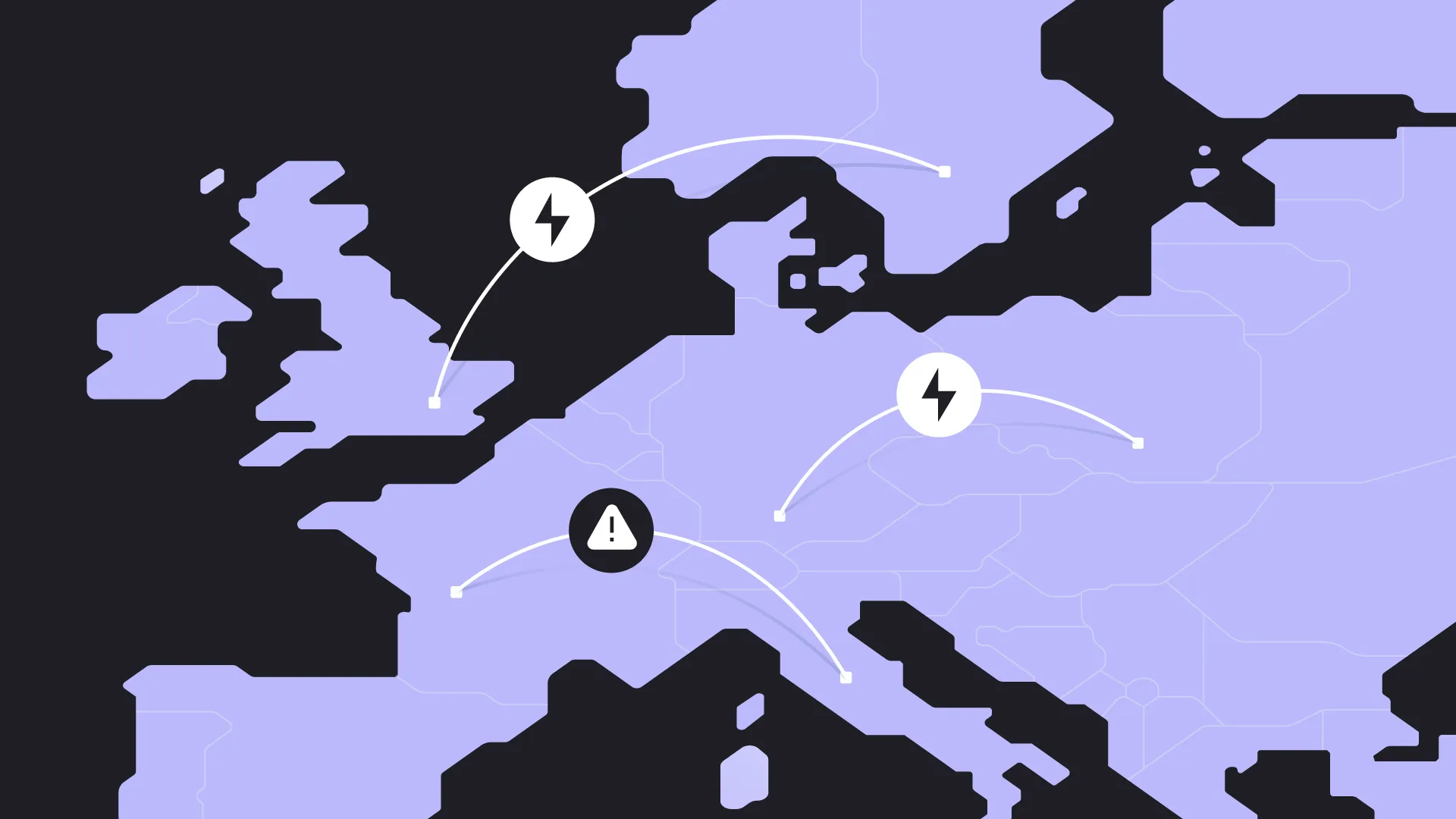

What’s missing? Removing cross-border obstacles

While the proposal addresses many of the barriers to instant payment adoption within the single market, one significant item remains: cross-border payments.

The SEPA Regulation, through Article 9, requires that all cross-border electronic payments in euros be as easy to make as domestic payments. However, IBAN discrimination continues to be a considerable problem, with banks continuing to decline cross-border SEPA payments (including open banking payments) at a far higher rate than domestic ones.

In addition, banks can impose obstacles in open banking authentication journeys that are often more cumbersome than for domestic payments. This leads to a higher proportion of users cancelling or abandoning the payment in frustration.

Examples of discriminatory steps in the payment process include:

Having to use a card reader to validate the payment

Having to register a non-domestic SEPA IBAN as a trusted beneficiary

Having to type in your own IBAN to make a payment

Restricting SEPA Instant payments only to domestic transactions

As instant payment will come by way of amendments to the SEPA Regulation, the EU should also use this opportunity to put an end to IBAN discrimination, including discrimination which impacts open banking.

What’s next?

In 2023, the European Parliament and Council will each consider the Commission’s proposal and may suggest changes to the SEPA Regulation. After they are passed, these changes will require an implementation period as well, so we’re a couple of years away from full availability of instant payments.

Still, addressing the issues above will enable cross-border instant payments. The single market is currently held back by the lack of instant payments, and this legislative proposal is one of the final key pieces to enable even more efficient borderless commerce across the EU.

)

3 tipping points for change within ecommerce payment experiences

)

How to reduce ecommerce cart abandonment

)