)

)

Open banking and instant payments go hand in hand. Through open banking, account to account (A2A) payments is fast becoming a competitive payment option in all sectors, even fast-moving ones like ecommerce or investment.

But consumers and businesses expect payment to be instant, convenient and certain, wherever they’re based.

In this blog post, we discuss why open banking payments will only fulfil their full potential in Europe if instant payments are available everywhere, and obstacles like IBAN discrimination are removed. We'll explain where we are right now on these issues – and what's coming up.

What is SEPA Instant?

SEPA Instant is a bank transfer scheme introduced in 2017 at the request of the EU, which was meant to enable easy and instant cross-border payments across 36 countries.

It was designed to take advantage of the 2012 SEPA (Single Euro Payments Area) Regulation, which is the legal basis for a pan-European space for bank transfers and direct debits.

“SEPA Instant was not supposed to be a premium service, only used in emergencies or as a last resort at a high cost.

But pan-European instant payments are at risk of fragmentation. Several national schemes were being developed or already adopted by the time SEPA Instant came around, such as iDEAL in the Netherlands or Swish in Sweden. These instant payment schemes do not operate across borders and cannot be the basis of one single, frictionless payments system.

SEPA Instant was not supposed to be a premium service, only used in emergencies or as a last resort at a high cost.

Rather, it was meant to be the foundation of a new EU normal, where instant and frictionless payments work the same way within country borders as across them.

Unfortunately, its limitations have turned it into a de-facto premium option.

Why is SEPA Instant important for open banking payments?

Open banking puts instant payments at the fingertips of both consumers and merchants. It integrates instant payments into regular business payment flows, elevating SEPA Instant from a bank transfer option available only through online banking to an alternative payment method in fast-moving sectors like ecommerce or investment.

Consumer demand

European consumers want payments that are instant, free and user friendly. They are more likely to trust businesses that process payments instantly. In industries like wealth management, half of consumers are likely to switch to a competitor that offers instant payments and one in three would consider spending more if they knew they could take out their money instantly.

Business demand

For businesses, instant payments mean better real-time visibility of cash and an improved cash flow. For ecommerce retailers in particular, it means less risk, since they can fulfil orders immediately (for comparison, online card payments take up to three days to settle).

Creating a competitive EU payment method

The European Payments Initiative was a recent industry attempt to create a single, consistent, and instant payment solution for retail use, based on SEPA Instant. It was meant to challenge incumbents such as cards, but it has recently scaled back ambitions significantly after more than half of the participants withdrew.

There is both room and need for a pan-European payments solution, one which is compatible with the open access principles of the Payments Services Directive (PSD2). Such a solution will be able to support a rich ecosystem of payment providers and provide maximum choice for consumers.

We support the EU taking action to improve the functioning of SEPA Instant. Adoption of A2A open banking payments will depend on the underlying instant bank payment infrastructure. Both merchants and consumers expect speed, convenience and security – all of which the combination of instant, cross-border SEPA payments and secure open banking APIs can deliver.

What’s the hold up with SEPA Instant?

SEPA Instant is optional: banks are not required to offer it, which means a little over half of EU banks make it available. Where they do, there are interoperability issues within countries and across borders.

Where it is available, it’s not competitive with other methods, and high transaction fees for consumers limit adoption: instant transfers are only 10% of all bank transfers.

Widespread IBAN discrimination also means that instant payments often do not work across borders.

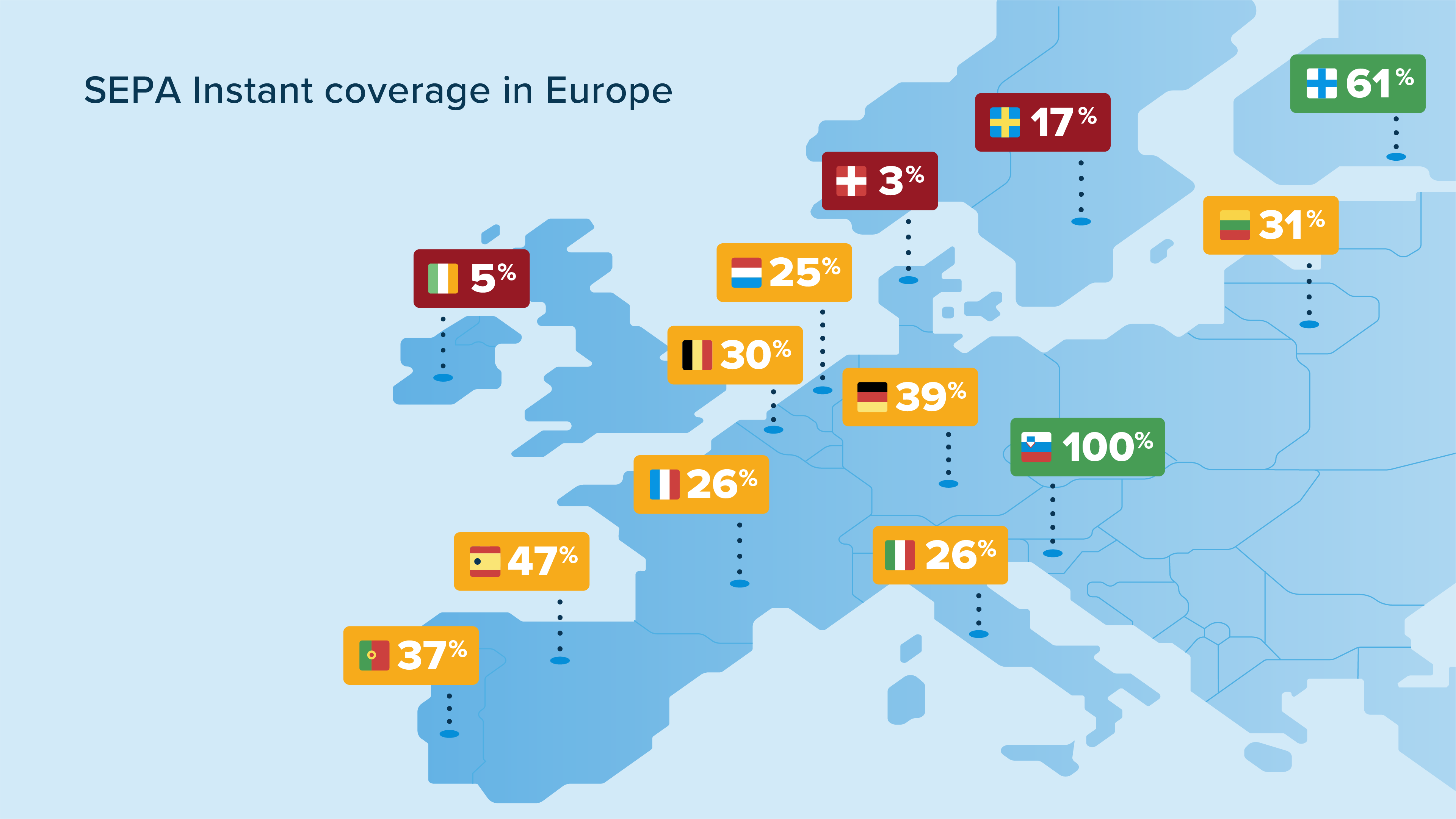

No mandate leads to low coverage

Coverage of SEPA Instant varies significantly between member states, from 100% in Slovenia to just 3% in Denmark. Slovenia is the first country where all banks that offer regular credit transfers also offer SEPA Instant, as of April 2022.

)

Interoperability of instant payment systems

Even high coverage rates can obscure the real availability of instant payments, because of the lack of interoperability for the two underlying ‘rails’ used by SEPA Instant, TARGET instant payment settlement (TIPS) and RT1. For example, nominal SEPA Instant coverage in France is 26%. In practice, this figure is much lower because some banks only use TIPS, whilst others only accept RT1 payments, causing a high rate of failure.

Sending vs receiving

There is an added challenge that a bank can fully adhere to SEPA Instant and still only allow consumers to receive SEPA Instant payments, not necessarily to initiate them. This is because the scheme is only focused on accounts being reachable for transfers by other banks.

Consumer fees

Where SEPA Instant is offered by banks, adoption remains relatively low. The main reason is that consumers are charged a fee for using it, making it less competitive against incumbent methods that are free, such as non-instant transfers or cards.

The fees vary by credit institution and from country to country. They range from flat-fees to basis-point fees. In France, a consumer is charged between €0.8 and €1 per transaction, while in Germany every transaction costs the consumer an additional €0.6 on average. In Spain, the flat fee can be as high as €12 per transaction.

| Country | SEPA Instant cost range |

|---|---|

| Belgium | €0.00 - €1.25 |

| Finland | €0 |

| France | €0 - €1.00 |

| Germany | €0 - €1.50 |

| Ireland | €0 - €0.99 |

| Italy | €0.60 - €5.90 |

| Lithuania | €0.41 |

| Portugal | €1.35 - €5.20 |

| Spain | €0.95 - €12.00 |

The practical result is that, wherever SEPA Instant it is available, adoption remains low. It has grown steadily since 2017, but it’s nowhere near its pan-European aspirations, going from 5.2% of all SEPA Credit transfers in October 2019 to 10.38% in September 2021 (and as low as 3% in some countries like France).

)

IBAN discrimination

The SEPA Regulation requires that all cross-border electronic payments in euros should be as easy to make as domestic payments. However, IBAN discrimination continues to be a considerable problem which affects all forms of payment.

In the case of open banking, it means that instant payments either cannot be initiated to a bank account from a different member state, or that banks create discriminatory, unnecessary steps which discourage the user and lead to high rates of abandoned or cancelled payments.

Examples of discriminatory steps in the payment process include:

Having to use a card reader to validate the payment.

Having to register a non-domestic SEPA IBAN as a trusted beneficiary.

Having to manually increase the account’s non-domestic transfer limit in the online banking channel – or by calling the physical branch of the bank.

)

The Accept My IBAN campaign has received over 2,000 complaints from consumers over the past year. Many more cases go unreported each year.

What are the next steps?

Because of SEPA Instant’s underwhelming performance, European Commissioner Mairead McGuinness announced in March that EU legislation on instant payments will be introduced in the second half of 2022. Instant and cross-border payments are also at the heart of the EU’s Retail Payments Strategy and an important building block for a pan-European open finance space.

We welcome this focus, and we’re committed to feeding into the discussions to make SEPA Instant and open banking work together to create a strong new EU payment method.

The following steps will be important for realising this goal:

Make sure all credit institutions can send and receive instant payments

Instant payments cannot be optional anymore. Credit institutions that offer regular credit transactions should also be obliged to offer instant credit options. This will lead to a much higher coverage rate across SEPA and in turn stimulate adoption.

Related to this is the ‘reachability’ gap which the EU must also address in order to promote adoption: adherence to SEPA Instant must include the obligation on banks to allow payments to also be initiated, not just received. The lack of interoperability for TIPS and RT1 must also be addressed as it obscures real SEPA Instant coverage.

To truly unlock cross-border instant payments, discriminating against IBANs from other SEPA countries must also become a thing of the past. We need more awareness of the phenomenon and stricter adherence to the SEPA Regulation.

Make sure that instant payments are free for consumers

Instant payments cannot be a premium service. Success will depend on them being free to consumers.

For instant payments to be truly competitive with other payment methods, transaction fees for the consumer must not exist. This is one of the most important ways to encourage adoption, as adoption is currently highest where fees are lowest.

Make sure consumers trust and understand instant payment protections

Consumers must trust the safety and reliability of instant payments. In turn, consumer interest will encourage merchants to offer bank transfers as a payment method.

Combining instant payments with secure open banking APIs gives us one of the fastest and most secure ways of paying.

Extra safeguards such as confirmation of payee can provide greater assurance to consumers that their payments are going to the intended recipient. These safeguards should be implemented in ways that do not discourage consumers by creating unnecessary obstacles in the payment flow.

)

TrueLayer part of FCA's Supercharged Sandbox to test agentic payments

)

Payment choice, not cards by default: the view on agentic payments

)