)

)

Introduction: Finding your perfect payments match

If you’re reading this, you’re at a critical stage in your journey to add open banking payments to your website or app.

As a payments product buyer, you likely know the problems with traditional online payment methods like card payments and manual bank transfers (high costs, high failure rates and poor user experiences to name a few).

You’ve reached the conclusion that the benefits of open banking payments can help you reduce reliance on other payment methods, reduce costs and fraud — whether that’s adding another option to your existing payment experience, or using it as the standalone payment method for your customers. And you’re ready to serve the 65 million open banking users there will be across Europe by 2024.

But how do you choose the provider that can build the right open banking payment experience for your business? The ever-evolving open banking landscape is an opportunity and a challenge. The regulatory picture is changing at different speeds in different countries, and finding a trusted partner is key to making the most of this technology.

This guide is designed to help you with that. It’ll walk you through each aspect you need to consider when choosing an open banking payments provider. From understanding the nuances of global coverage to knowing exactly how to integrate open banking payments into your customer journey, this guide covers it all.

Haven’t quite reached this stage in your open banking journey just yet? Start with our comprehensive guide to open banking to get to know open banking, and how it can benefit your business.

Before you get started

While this guide is designed to help you better understand what questions you need to ask your provider, one question you should ask yourself is: “What am I trying to achieve with this new payment experience?” Without that clarity in mind, it can be hard to focus on the most important questions and the answers you need.

Remember, once you’ve shortlisted your providers, the next step is often a request for proposal (RFP) or request for information (RFI). These tasks can take weeks or even months, so having the goal always in mind will help you reach the end of that process with a chosen provider who can deliver exactly what you need.

A note on terminology

For the purpose of this guide, we’ll refer to the payment method as ‘open banking payments’ because PSD2 legislation — commonly known as open banking — made this payment method a reality.

However, this isn’t necessarily how you should name the payment method when speaking to customers. Instant bank payment, instant bank transfer, and pay by bank have become common customer-facing ways to describe an open banking payment. A good provider will guide you on the right naming conventions to increase customer adoption. More on that in Payer experience.

How to use this guide

The buyer’s guide to open banking payments is your playbook for finding the right open banking payment partner for your business. With it, you can better understand which aspects of the overall payment experience are key to your brand’s success.

The guide is broken down into seven sections, each covering a part of the selection process.

Coverage

Understand how coverage — where you can take a payment or pay out through open banking across the globe — should be defined and measured, along with the complexities and quirks of different markets.

Features and functionality

The ability to collect a payment or allow your users to fund their accounts are table stakes for open banking. But there are so many other potential features throughout the lifespan of a payment that could improve your brand’s payment experience.

Integration options

How you add open banking payments to your app or website will depend on your developer resources and how quickly you want to go to market. Get to know what integration options are available and which is right for you.

Payer experience

Your open banking payment method is only as good as the customer’s experience when paying. Learn how the right provider can help you design open banking payment journeys that increase adoption and conversion.

Stability and security

Can you rely on your provider to help you build a payment experience that is both reliable and safe for your business and customers? Understand how to judge the quality of a provider’s testing and security regimes.

Ongoing support

A good provider will help you launch a payment experience that works from day one. But ongoing support — both reactive and proactive — will be the mark of a long-term partnership with a provider.

Provider expertise

While you might get all the right answers to your questions, can you trust your provider to deliver? Discover how to evaluate your provider’s expertise, experience and track record.

)

Chapter 1: what does coverage mean and why is it important?

At its most basic level, coverage is the proportion of your existing and potential future customers that you can collect payments from, and potentially pay out to, using a particular provider. It’s critical to be able to serve as much of your current and future customer base as possible with your payment experience.

But open banking coverage isn’t as simple as it first appears. Not all coverage is created equal, and different providers measure coverage in different ways, making it tricky to directly compare two providers.

For a true reflection of coverage, there are four angles to consider*:

Banked population

Type of accounts

The type of coverage

The quality of coverage

)

*If you want to send money to customers, as well as collecting payments, then use this same framework for payouts and withdrawals.

Banked population

How would you measure coverage? The number of people within a market that can use the payment method? In the case of open banking payments, that is the ‘banked population’, and it gives a true reflection of the breadth of coverage you can hope for in a given country. Some providers use the number of banks or even the number of bank branches. While thousands of bank branches sounds like a big number, it may only represent a fraction of the banked population.

)

Personal accounts or business accounts

If access to businesses is important to your brand, then make sure you know the coverage for business accounts, too. For many providers it’s often lower than with personal accounts.

The type of coverage

Adding open banking to your website or app is often a choice between application programming interfaces (APIs) and screen scraping. These are the two main ways your provider can connect to the banks.

APIs are a secure way to connect. Payers authenticate their payment directly with the bank using strong customer authentication (SCA), and APIs typically enable app-to-app user journeys on mobile phones. In the UK and Europe, open banking APIs are highly regulated under PSD2 legislation for added security.

Screen scraping, on the other hand, involves a customer sharing their bank account login details with the open banking provider, which stores them unencrypted on the server doing the screen scraping.

With screen scraping, there’s a much higher risk that confidential customer information can be leaked, and the very process is often a violation of a bank’s terms and conditions. From a business’ point of view, screen scraping is time consuming to maintain, as even the smallest update to a bank webpage can completely disrupt or outright break the user experience.

Providers that use screen scraping might say it performs better than APIs. And it’s true that, in some countries, API-based open banking journeys are still evolving and haven’t yet reached their full potential. But it’s important to future-proof your payment collection. Screen scraping has been deemed unsafe by regulators across Europe, and plans are in place to eventually ban it while the API approach is heavily backed by regulators.

The quality of coverage

While APIs provide a better experience for all parties, there can still be a big gulf in the quality of bank APIs. A provider may be connected to a bank through an API, but that doesn’t mean they are pushing much traffic through it or testing it.

For markets that are vital to your business’ operations, consider a provider that has a significant testing regime in those areas. They should be processing high volumes of requests through the relevant APIs to understand bugs and edge cases.

Providers should also be sharing findings directly with the banks to help them improve API quality and reliability, to the benefit of businesses and their customers. Under PSD2 rules, banks are required to fix technical issues, so an active feedback process will benefit your business.

How does TrueLayer compare?

TrueLayer covers more than 95% of bank accounts in major European markets – for example, 98% in the UK, 99% in Spain and 95% in Ireland. Our coverage is constantly growing across Europe.

TrueLayer’s coverage in the UK and Europe is 100% API-based, meaning we don’t use screen scraping. At TrueLayer, we invest a huge amount of time and resources in testing bank APIs, debugging and sharing our findings with banks to help them fix issues and improve their API quality, while minimising the impact for our clients.

Chapter 2: what open banking features are available and which do you need?

An open banking payment, at its core, allows a customer to pay for something online straight from their bank account.

That could be buying a product from an online store, or topping their account up with funds on a wealth management app, pension app or iGaming platform. This is one of the core aims PSD2 was designed to deliver on — a secure and instant way to make payments online without a physical plastic card.

That’s the minimum. As open banking evolves, there will be more functionality available throughout the lifecycle of a payment. From the moment a website visitor decides to become a paying customer, along with any verification needed, to the point where they request a payout, withdrawal or even a refund, these features can improve the overall buying experience.

When choosing your provider, think about the following features and how important they are to your new payment experience.

Account verification

In industries like iGaming and financial services it’s important to confirm your customer’s identity and the ownership of their bank account. Account verification via open banking connects your business to your customer’s bank account to fetch financial information via secure APIs. This validates that your customer owns the bank account in question, without the need for manual bank statement uploads or micro deposits, vastly reducing the chances of fraud or the risk of a customer making a payment to an incorrect account.

Refunds

Refunds have been considered the Achilles’ heel of open banking, as the in-built solution, known as reverse payments, has a poor customer experience. Reverse payments introduce unnecessary friction into the user flow and need to be approved by someone in your business. To meet customer demands, some providers, including TrueLayer, have built on top of basic open banking infrastructure to make automated, instant refunds possible — all within a closed-loop system. In fact, 81% of shoppers expect a refund from an online purchase in a week or less.

Payouts and withdrawals

Whether it’s to withdraw their funds from an investment app or iGaming provider, or even to process the sale of their car, the ability to pay your customers instantly is another way to improve the end-to-end payment experience. Instant bank payouts and withdrawals also build trust. Almost half of current investors (46%) said they were likely to switch providers for instant withdrawals, while 37% would also consider depositing more money if they could withdraw instantly. Not all open banking providers process payouts, so be sure to ask.

“We know from our customers’ feedback that having instant access to their funds is a key motivator to use our brands. Customers can deposit money instantly so why not be able to withdraw instantly too?

Natalie Dunne, Director of Payments

Sweeping

Known as ‘me-to-me’ payments, sweeping in the UK enables the repeat transfer of money between two accounts belonging to the same person. If your business involves helping people budget, save or invest, the ability to easily transfer money between accounts they own on a recurring basis is highly beneficial. As UK banks are required to build variable recurring payment (VRP) APIs, sweeping is quickly becoming a feature your provider could offer.

Please note: this functionality is not yet mandated by regulators outside the UK.

Recurring payments

While VRP has only been mandated for sweeping in the UK, several UK banks are choosing to go beyond what is mandatory and build APIs that will enable more kinds of recurring payments. If your business would benefit from offering subscription payments, recurring invoices, instalments or payments that are typically handled by card-on-file, open banking VRPs could become a powerful alternative to continuous payment authorities (CPAs), card-on-file, and direct debit.

Payment statuses

Knowing whether a payment has 'completed' or 'failed' — or 'sent' in the case of a refund or withdrawal — lets you quickly identify customers having payment issues. Combining this with specific error codes for why a payment has failed makes rectifying payments problems much quicker and easier. Statuses are also helpful to update the end user, removing any ambiguity about whether they have successfully made a payment.

Information and insights

Having a more complete view of your customer’s financial data — think balances, transaction history and credit limits — can improve your product offering. Account information services (AIS) can be used separately to payments, but when combined can enable powerful functionality like affordability checks, VIP customer segmentation and savings & investment insights.

Plus: a clear plan for emerging use cases and technology

Open banking is becoming a widely-used payment method across Europe, with an estimated 28 million users (more than 6 million of those are in the UK alone), the technology and regulation is changing and evolving all the time. Your open banking provider should be building and testing solutions for these new use cases, especially where an emerging use case could benefit your business.

How many APIs do you need to integrate with?

If your brand needs a selection of features, you may need to integrate with several APIs. For example, if there is a separate API for each product and each market, it can quickly multiply the time and resources needed, possibly derailing or prolonging the integration process.

How does TrueLayer compare?

TrueLayer offers solutions for the entire end-to-end payment experience, including payments, refunds, payouts, withdrawals, VRPs in the UK, and merchant accounts from a single Payments API. Account information and verification are also available via additional APIs. We carried out the first ever live VRP transaction with NatWest in the UK and are in regular communication with regulators to help ensure VRPs are as powerful as possible.

Chapter 3: what integration options are available and which should you choose?

Building your open banking payment experience is not simply about finding a provider that offers the right coverage for the right products and features.

It’s also about finding one that can work with your available development time and expertise, as well as working with your existing tech stack.

The integration process — by which we mean the process of turning your proposed payment experience into a working system that your customers can use — should be quick, match what was promised during the sales process and result in a high-converting payment option that your customers actively choose.

Ways to integrate your new payment experience

There are several ways to connect your new open banking provider to your business. The most common way is with an API. This could be a direct integration or via a partner — like a payment service provider (PSP) — that already powers your existing payment methods. The API could be delivered via a software developer kit (SDK) or hosted payment pages (HPP) depending on what you want your payment experience to look like and how much developer resource you have available.

The route to integration can seem daunting, but a good provider is there to guide you through this decision-making process and give you advice on what type of integration will help you deliver your intended use case on time. For example, direct API integrations allow customers to have a fully customisable payments flow, but it requires more time and technical expertise to set up. On the other hand, integration tools such as HPPs, SDKs and client libraries are slightly less customisable, but all make the integration process much smoother and easier for developers.

Self-serve style options do exist — where you are essentially given access to raw open banking data — but for most businesses, the lack of guidance creates ambiguity and obstacles.

How long should the integration process take?

Any integration process involves actions from both your provider and your business, so a delay from your side — be it lack of developer resource, other priorities, etc — will add to the time it takes. But a good direct integration, where both sides are able to focus on the process and have agreed on the deliverables, should take around six weeks from kick off to go live. On top of that, using SDKs and HPPs could save an additional one or two weeks of integration time.

Consider the pain points that have led you to choosing an open banking payment provider. If you think the results of adding a new payment method will result in significant savings or will improve conversion, then finding a provider who can help you integrate swiftly should be a top priority.

Clear stakeholders and deliverables

A provider will often assign an integration specialist to help build your integration. They may be called Integration Support, Integration Sales or Solutions Engineering, but their job will be to guide you through the process, as well as build and execute an integration timeline.

A good integration project will include a full list of stakeholders, deliverables and milestones. This process will typically begin during the sales process, so there’s no delay in launching your open banking experience if you commit to that provider. You should be left with no questions over which tasks should be done by which party, and in what order they need to be completed.

Advice and best practice

As well as being a conduit for your needs and requirements, best-in-class integration support will give expert advice on how to make your new payment experience as effective and efficient as possible (see Payer experience). An established provider will have carried out hundreds of integrations, learning what works well and what doesn’t for different use cases, industries and business models.

One common objective for any new payment experience is to maximise conversion rates, meaning the percentage of customers who complete a payment journey once started. Your integration team should be able to advise you on how to build a payment flow that increases conversion.

How does TrueLayer compare?

TrueLayer will assign an integration expert to your business, and you will typically have two-to-three meetings with them during the sales process so they can design your ideal integration. They will provide you with best-practice integration advice and support throughout the process, including:

Guiding you through which type of integration is right for your use case, taking into account your end-goal, plus the level of technical resources you have available.

Mapping out the integration process, from both a user’s point of view and a back-end technical perspective.

Delivering UX guidance to support you in delivering the best payer experience to boost conversion and share of checkout rates (see Payer experience).

Creating and running check-ins with you throughout the integration phase to drive the integration forward on schedule and help with any technical issues.

Working with your customer success manager and other post-integration stakeholders to create and prioritise feature requests (see Ongoing support).

“Overall, we had a great experience integrating with TrueLayer. They had good developer docs and Zendesk support, and their developer console was easy to use.

Harry Wynn-Williams,

Senior Software Engineer

)

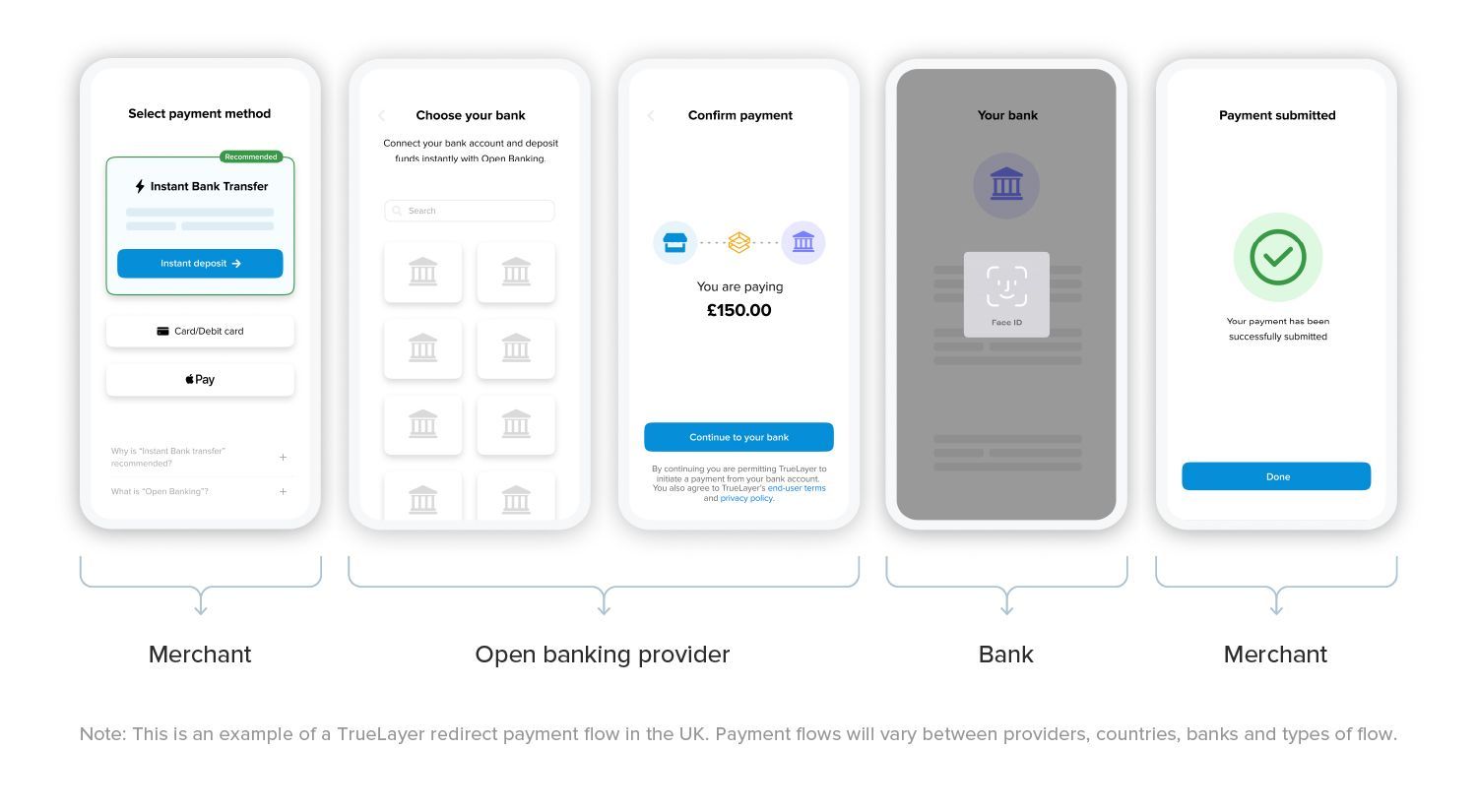

Chapter 4: why is payer experience so important?

Payer experience (also known as customer experience or user experience) is the quality of the customer’s experience when using an open banking payment.

A poor payer experience can lead to your customer not choosing or abandoning the payment.

For customers to choose open banking payments over other available payment methods, your provider needs to take into account four key factors that affect your customers’ perception of an open banking payment:

Convenience: will this take long?

Clarity: what exactly do I need to do? Is it going to be difficult?

Familiarity: have I done this before? Do I recognise it?

Security: is this safe? Do I trust it?

)

They then need to navigate the open banking payment flow successfully. A completion of a started payment flow constitutes a conversion. Good UX practices can also increase the likelihood of a user completing the payment. Best practices for this include:

💡 avoid ambiguity

👀 be transparent

☝️ use common patterns and shortcuts

✏️ simplify complexities

)

It’s important to note that part of every open banking payment journey — the authorisation step — is dictated by the banks, rather than the provider you choose, and that standards set by governing bodies across Europe can lead to inconsistent user journeys.

)

But your provider should be able to advise you on how to build a high-performing payment journey, taking into account the nuances of different banks and different market standards across Europe, as well as the needs of your business. Your chosen provider should be able to help you with:

Tried-and-tested bank selection and consent screens

The two parts of the open banking payment flow that your provider will control are the bank selection and consent screens.

Bank selection screen: the user chooses from a list of available banks (at which point they are redirected to that bank to authorise the payment).

Consent screen: the user is informed of the information required of them to complete the payment process, and they give their consent.

Your provider should have tested and optimised screens for both of these parts of the payment flow, which meet regulatory requirements, and they should give you recommendations for your business and use case.

Expert advice on authentication flows across Europe

As we mentioned in Coverage, payment flows will differ across Europe, as banks apply different standards for UX during the authentication part of the flow. While your open banking payment provider can’t control these parts of the journey, they can advise you on what markets and banks have particular UX quirks, such as if a specific bank requires IBANs or specific error messages to be aware of. They should also advise on how to build your flows to account for these differences.

Your provider should also be in constant communication with banks and regulators, feeding back to them and lobbying for improvements.

High performing end-to-end payment or deposit flows

The parts of the payment flow controlled by your provider, the parts controlled by the bank and the parts controlled by your business (eg payment selection screens and success screens), combine to make the end-to-end payment or deposit flow.

While distinct, they naturally all work together to drive a user to complete a payment. Your provider should be able to advise on how to build a full flow that works effectively, removing ambiguity and complexity that would increase the chance of a payer dropping out of the flow.

)

Best practices for driving open banking adoption

Adding open banking payments to your payment page isn’t simply about what happens when a payer has chosen open banking. It’s equally important to ensure your customers understand what it is and what it offers them compared to other available payment methods.

A provider should be able to advise you on the language to use (ie what to call your payment method) and how to structure the hierarchy of your payment options to increase the share of checkout (the percentage of all a business’ payments transacted through open banking). This is particularly important if further open banking adoption drives down your costs and operational inefficiencies.

)

How does TrueLayer compare?

TrueLayer offers both direct API integrations that allow for customised payment flows as well as hosted payment pages (HPPs) and mobile software developer kits (SDKs) with some customisable elements and developer libraries.

Plus, our new QR code authentication feature lets you authorise desktop payments faster by handing off the payment session to the customer's mobile banking app via a QR code.

Our Integration Support team will work with you during the sales and integration process to guide you through the best payment flow for your use case while taking into account available development time.

Through extensive testing, research and experience of previous integrations, our UX experts have built payment flows that are fully optimised for conversion, with continuous testing always ongoing to find further optimisations.

Chapter 5: why is stability and security important in open banking payments?

Open banking in Europe came into force in 2018, and while the technology powering open banking payments has advanced significantly in that time, it is constantly being iterated upon and improved.

And if you want to offer open banking payments to your customers, it’s vital to find a provider with stable APIs (ie APIs that virtually always work) and good security, so neither you nor your customers are at risk from cyber criminals. They should be continually testing, debugging and maintaining both their own products and the bank APIs they connect to so you know your new payment method will continue to offer a good payer experience over time.

When assessing stability, look out for the following:

A detailed API status page

Your potential payment provider should have a publicly available status page, which will detail the uptime of each API. Some providers will show uptime in hourly increments, while others will show daily increments. You should also be able to look at historic status updates to get a sense of how consistent the provider’s APIs are, as well as how long any downtime typically lasts.

)

Minimal downtime

With even the most stable of APIs, downtime can and does happen. But your provider should be able to clearly communicate to you what caused a particular period of downtime. For example:

Was it scheduled maintenance or an unexpected problem?

How long did it take to discover

How long did it take to fix?

How many end customers were affected?

How were end customers notified of any problem?

What work has happened to prevent this type of problem in the future?

A clear methodology for testing and monitoring bank APIs

While your provider can control the reliability of their own service, bank APIs are outside of their direct control. And as discussed in Coverage, they have different levels of reliability.

With that said, your provider should have a clear process for testing the different bank APIs it connects to. If a particular set of banks — banks in a specific country, for example — are critical for the success of your payment experience, then make sure your provider regularly pushes large volumes of requests through those APIs and has a clear process for delivering feedback to the banks on how they can improve.

A rigorous information security programme

To keep you and your customers’ financial data safe and secure, your open banking payment provider should have:

A consistent threat modelling programme, mitigating any potential vulnerabilities

A dedicated security team

A security programme based on a recognised standard (eg ISO27001)

Independent third-party auditing of its security programme

A clear protocol for release management

Oversight of any third-party development, with the same level of testing as internal teams

An independent third-party penetration testing programme of its infrastructure

While it’s difficult to pinpoint one single area of information security that’s most important, the consistency of the answers from your intended provider will give you a sense of how strong their security approach is.

How does TrueLayer compare?

TrueLayer systems operate with over 99.9% uptime, and you can see live status updates for all APIs on our status page. Our connections to bank APIs across Europe are constantly being tested with high volumes of requests to spot errors and feed back those issues to the banks.

We carry out all our development work in house, and we have a dedicated Information Security team. We are also fully ISO27001 certified.

We operate a 24/7 technical on-call rota composed of engineers involved in the development of our systems and the availability of our service.

In the event that our monitoring detects a potential issue with one or more of our systems, our on-call engineer will be automatically paged to triage and resolve any potential issue. Having this 24/7 coverage ensures the impact of a loss of service is minimal and resolved quickly.

Chapter 6: How will your provider maintain and improve your open banking experience?

While a quick and straightforward integration process should be a key factor in your choice of payment provider, the relationship doesn’t end once the integration is complete.

It’s just as important for your business to easily operate and understand any new payment experience, as well as getting useful analysis, so you can further improve and optimise. You should also be able to give feedback to your provider for potential improvements.

Combining easy integration, an ongoing relation and a strong feedback loop will create a high-performing payment experience.

But things do inevitably go wrong from time to time. Your provider should also have dedicated reactive and proactive support to help solve any issues, averting any potential crises.

Customer success management

A customer success manager (CSM) will often be your business’ main point of contact as you take live your new payment experience. They will also help you identify and explore new benefits and new opportunities to drive incremental value for your business.

A CSM is a key part of what strengthens a relationship with a provider, advocating for your business’ needs internally and helping you build a roadmap for long-term success with your open banking payment solution.

Having a CSM assigned to your account will likely depend on the volume of payments your business processes, so carefully consider how important this service is to your business.

Client care

Client Operations (also known as Client Care or Customer Support) will be your first point of contact when things go wrong. They can fix some problems quickly to avoid major issues, or triage the problem to the right team. When assessing your potential provider, consider the following points:

Technical support: are there dedicated support engineers for technical problems?

Available languages: can your provider help your team members across the globe regardless of the language they speak?

Opening hours: In case of an emergency, when is support available? And how can you contact support outside of typical Monday-to-Friday working hours?

Response times: how quickly will support respond to and resolve any issue? Is their support model ‘tiered’, meaning critical and wide-reaching issues are prioritised?

Levels of support: does your provider offer different support packages at different price points? Can you ‘run out’ of support?

Information helpdesk

Having the option to speak to customer support provides peace of mind. But it’s also inefficient to call or email support for information for every minor question. A regularly updated helpdesk, which contains answers to commonly asked questions, is useful for any team members involved in the day-to-day operation of your payment experience.

API reference documentation

Often shortened to ‘docs’, API reference documentation is the technical library with everything your development team will need to know about your provider’s API. While having integration support is key, it’s equally important to have a well-organised set of content so your developers can self-serve and move as quickly as possible.

“"It couldn’t have been easier. TrueLayer’s customer service is amazing. Any questions were answered practically immediately, and our developers were able to integrate quickly and seamlessly."

Irakli Agladze,

Head of Open Banking

)

How does TrueLayer compare?

TrueLayer has dedicated Integration Sales, Customer Success and Client Operations teams to launch, operate and optimise your new payment experience — and to help if things go wrong. Help is available 8am–8pm GMT, with support available in six languages.

We also have clear processes for issues depending on what proportion of users they affect. For example, we aim to respond to critical incidents within 30 minutes and provide a resolution within four hours of being contacted by the customer.

The TrueLayer helpdesk can be found here. Our API reference documentation can be found here.

Chapter 7: how to judge a provider’s expertise and experience

By speaking to your shortlisted providers and asking them the questions outlined in this guide, you should be able to find the perfect partner for your business.

But there’s one key element of the equation still missing: does your provider have a track record of delivering on what they promise? Or to put it another way, does your provider have the experience and expertise to deliver the ideal payment experience for your business?

While providers will inevitably talk up their expertise, there are a few ways to understand whether your provider can build the payment experience you need.

Reference clients and case studies

Case studies are a great way to get real-world insight into your payment provider, directly from other customers who also use them. The most important case study you can request is one that matches your use case.

This proves your provider can build the solution you need. Other aspects, like case studies from similar industries and similar-sized companies, add extra context and reassurance, but offer little value if the use case is different.

Third-party reviews and NPS score

While case studies provide evidence that your provider works with brands similar to your own, all providers will inevitably choose case studies that reflect well on their solution.

For an unbiased view from other merchants, look at software comparison sites like G2, and for end-consumer opinions, look at TrustPilot.

Net promoter score (NPS) is another measure to look at. Businesses use it to track the likelihood of customers recommending a brand to a friend or colleague. A positive NPS score is a sign of a generally satisfied customer base, while 50+ is considered excellent.

Active participation in the open banking ecosystem

Your provider’s ability to meet your current requirements is crucial, but it’s also worth considering what future opportunities and threats your business could face. With the open banking landscape evolving all the time, is your provider an active participant in shaping the landscape? Look out for evidence of your payment provider participating in working groups, and engaging in active dialogue with regulators and governments.

Financial stability

Business continuity is a big factor when taking on a new supplier. Can you be sure that your provider has sufficient funding and/or cash reserves to operate for years to come? Have they taken on VC funding, are they bootstrapped, or are they funded by debt financing? Your provider should be transparent about its investors, long-term plans and its financial outlook.

How does TrueLayer compare?

TrueLayer is backed by leading investors, including Stripe, Tiger Global, Tencent, Addition, Temasek and more. To date, we have raised $270 million in funding to allow us to take open banking payments mainstream. You can read case studies from our customers across several industries. Companies we’ve worked with include:

TrueLayer also has an active policy team that regularly lobbies regulators for open banking improvements that benefit both businesses and consumers. We’re involved in several working groups including the Payment Systems Regulator ‘Digital Payments’ working group and EU API scheme working group (SPAA MSG).

“We see TrueLayer as a world leader in the open banking space. Like us, they have an aggressive roadmap that touches many different aspects of open banking.

Joshua Fernandes,

Former Open Banking Product Owner

)

Chapter 8: your open banking payment provider checklist

Now that you’re armed with the knowledge to make your decision on an open banking payment provider, it’s time to evaluate your potential providers.

Below is a handy checklist to ensure you have all the information you need to make an informed decision on your open banking payment experience.

1. Coverage

- You know what markets your provider covers and the % of the banked population in each of those markets.

- If business accounts are important, you also know what markets your provider covers and the % of the banked population in each of those markets, specifically for business accounts.

- You know whether your provider uses APIs or screen scraping. If they use screen scraping, you also know their plans for expanding API usage.

- You know how much and how often your provider tests their APIs, and how they feed this information back to the banks.

2. Features and functionality

- You know the products and features your provider offers, which are important to your use case.

- You know where these products and features are available, and if they are in general availability or early access.

- You know which new technologies and features are on your provider’s roadmap, and when they will likely be available.

- You know how many APIs you will need to integrate with for your use case in all your chosen markets.

3. Integration options

- Your provider has advised you on the different integration options, and recommended the best route for your requirements.

- Your provider has advised you on the expected timeline of your integration.

- Your provider has provided you with a full breakdown of your integration process, with clear stakeholders and deliverables.

4. Payer experience

- Your provider has optimised bank selection and consent screens to include in your payment flow.

- Your provider has explained on different bank authentication flows, and talked you through their process of directly advising banks on ways to improve UX.

- Your provider has recommended ways to improve the end-to-end payment flow to increase conversions.

- Your provider has a testing programme for continuous UX improvements.

- Your provider has advised you on how to increase open banking payment adoption on the checkout or payment page.

5. Stability and security

- You have access to a detailed and regularly updated status page. You know the provider’s uptime in the last six months.

- Your provider has given adequate explanations for any recent downtime or lack of service.

- Your provider has explained their devsecops programme and shared relevant certifications.

6. Ongoing support

- You know if and when you will be assigned to a customer success manager.

- You know when and in what languages general and technical support is available.

- You know how long it will take to respond to and resolve critical issues.

- You have access to a self-serve helpdesk and API reference documentation.

7. Provider expertise

- You have seen case studies or testimonials from businesses with a similar use case to your own.

- You have seen customer ratings from G2, TrustPilot or similar.

- You know how your provider is funded.

About TrueLayer

Build better payment experiences

Accept and send instant bank payments in any app or website. Cut costs, fight fraud and get money moving fast.

The complete open banking payments solution

Instant pay-ins: let customers top up their accounts, purchase products and send money. In seconds

Instant withdrawals & refunds: automate sending instant refunds and withdrawals to your customers

Variable recurring payments: collect recurring, ad-hoc and variable payments securely

Ready to get started?

Talk to one of our open banking experts or book a demo at truelayer.com/contact

)

TrueLayer part of FCA's Supercharged Sandbox to test agentic payments

)

Payment choice, not cards by default: the view on agentic payments

)