In conversation with Freetrade: opening up investing

)

)

Tell us about Freetrade.

Freetrade is an app-based brokerage platform offering simplified and commission-free investing. Stock investment is complex, expensive and out of reach for lots of people due to opaque charges and clunky user experience. It’s our mission at Freetrade to get everyone investing, and we aim to do that by simplifying the investment experience and providing transparent upfront pricing.

How has the pandemic impacted your business?

When lockdown started, we thought we’d see a reluctance to invest, but we saw the opposite. Customers perhaps were travelling and spending less, and had more time on their hands to wonder what to do with their disposable income. As a result we’ve seen record growth in customer numbers and trading activity. We consistently rank in the top two retail brokers for daily volume of orders on the London Stock Exchange and we’ve recently passed 700,000 customers. The average customer portfolio size has also grown from about £1,000 to £2,000.

What led you to TrueLayer?

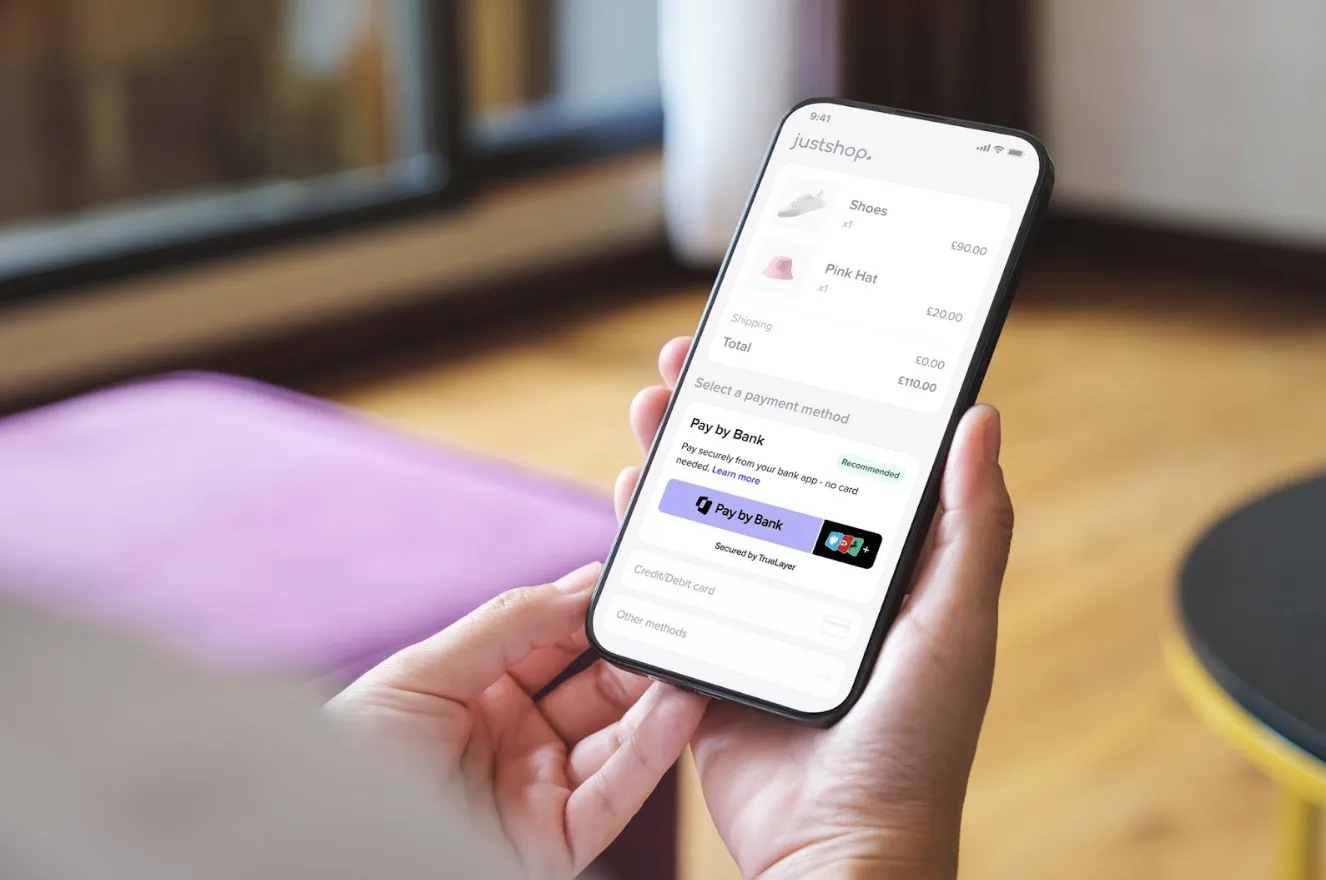

Before TrueLayer, manual bank transfers and card payments were the only two methods we offered to fund an account. Bank transfers were far more popular, but required customers to copy and paste between online banking screens, which led to friction and mistakes at a crucial stage in the customer journey.

On our side that led to a lot of operational strain while we tried to reconcile payments — matching unallocated deposits with accounts. For the customer, if they didn’t drop out, they might have had a poor experience waiting for funds to be credited, and end up contacting us to find out what was happening.

The pain was growing with the business – more and more deposits were ending up in that unallocated pool. Card deposits don't suffer from the same issues but they’re more expensive to process.

How does TrueLayer help?

By using TrueLayer’s open banking API we get the best of both worlds — there’s a simplified in-app deposit flow, with cost-effective processing. Customers can make payments quickly, and for us, the payment parameters are all there and can be automatically allocated.

How has your customer community reacted?

The old process was effectively a black box where we didn’t know when the customer might have actioned their payment; and they got no feedback at all until the payment landed in our account and was allocated.

The in-flight experience is much better now. Existing customers are adopting open banking to make deposits, and new customers are reporting payments going missing far less often.

If we look back at our first two full months of data, in September, open banking payments made up a third of all deposits. Now, they’re more than two thirds.

Last year we saw a 60% increase in the total value of open banking deposits, while the total number of open banking transactions went up by 35%, and the average transaction size increased by 18%.

How do the results compare with expectations?

Reducing unallocated deposits was our main motivation — at one point as much as 10% of monthly deposits were unallocated. That might mean us sending back £300,000 each month to customers for deposits we couldn’t match. That’s a lot of money customers have committed and it’s a bad first experience if we have to send it back.

With TrueLayer we’ve reduced our total unallocated deposits to 2% and I’m hoping we can optimise it even further. We’ve also made significant cost savings by reducing card payments to 5% of total deposits.

What impact will open banking have in wealth management?

We’re increasingly moving to a mobile-first, app-based world, where customers expect complete visibility over their finances. Nowadays, however you choose to distribute your wealth, there’s an expectation that these different systems and accounts can talk to each other, and display disaggregated views of your finances — and that you can move money freely between those pots. That’s especially important if you’re moving large sums, as is often the case with wealth management.

Open banking helps us to meet that demand and facilitate those quick and simple money movements so people can react to investment opportunities.

Finally, what’s coming up for Freetrade?

Here are some of the key features we’re working on currently, but we’ve also got a lot of surprises on the way!

Continuing to expand our investment universe with more stocks and ETFs

Rolling out Freetrade to Europe

Trading the biggest European shares and ETFs

)

How does your business stack up on the Pay by bank value flywheel?

)

Payment incentives: the secret sauce in your Pay by Bank recipe

)