)

)

Many companies require customers to undergo bank account verification before they can use a product or service. Whether it involves older methods like checking a bank statement or newer innovations like open banking, it’s an important step in ensuring customers’ funds end up in the right place. In fact, it’s often a key barrier to fraud and costly mistakes.

So what is bank account verification, and how does it protect businesses and consumers? This article will explain the basics, outlining different methods available so you can determine which bank account verification system best suits your needs.

What is bank account verification?

In short, bank account verification is a way to check that a customer using your service is the same person named on the bank account they’re paying from. It usually involves the customer providing credible information that proves their account ownership, such as a bank statement.

In some cases, consumers can prove their identity by providing data that matches the data on file at a credit bureau or held with their bank.

Why is bank account verification important?

Bank account verification is important for a number of reasons, not the least of which is fraud prevention. With fraud losses related to remote banking, payment cards and cheques accounting for a loss of over £708 million in 2023, it’s more important than ever for companies to protect their customers.

Compliance is also a significant factor. In many industries, companies have a regulatory obligation to verify account holders’ identities. Companies can include account holder name checks as part of their processes for anti-money laundering (AML) and know your customer (KYC) processes.

In fact, keeping customers safe is a major part of providing a positive customer experience. A survey from Entrust found that nine in 10 respondents expressed concerns about credit or bank fraud. Verifying bank account information can reassure customers that a merchant is reputable and their information is secure.

Bank account verification can also prevent human error such as somebody inputting their bank account details incorrectly. At best, these mistakes can cause a payment to fail or bounce, creating friction and frustrating customers. At worst, they can send a payment to the wrong account, putting a consumer’s funds in jeopardy. By relying on an effective bank account verification system, businesses can prevent both of these outcomes.

How do you verify a bank account?

There are many bank account verification methods that businesses rely on to validate their customers’ account information. These include:

Micro deposits: a customer gives their account details to a merchant. The merchant then sends two minuscule deposits to the customer’s account to verify its ownership.

Sending bank statements: a customer provides a merchant with documents from their bank. These statements list the customer as the account owner, proving their identity.

Credit checks: a merchant checks their customer’s account details against the information held on file at a credit bureau. If the information matches, the account is verified.

Open banking: by partnering with an open banking provider, a merchant connects directly to their customer’s bank account in real time. The provider then instantly compares the customer’s name and account number with the details listed with the customer’s bank.

How long does it take to verify a bank account?

Bank account verification can take as little as a few seconds and as many as 10 days, depending on the method used.

Open banking verification and credit checks each involve electronic checks against accounts in real time. As a result, they can confirm a customer’s account details immediately.

| Verification method | Time taken |

|---|---|

| Micro deposits | 1-2 days |

| Bank statements | Up to 10 days |

| Credit bureaus | Instant |

| TrueLayer Account Verification | Instant |

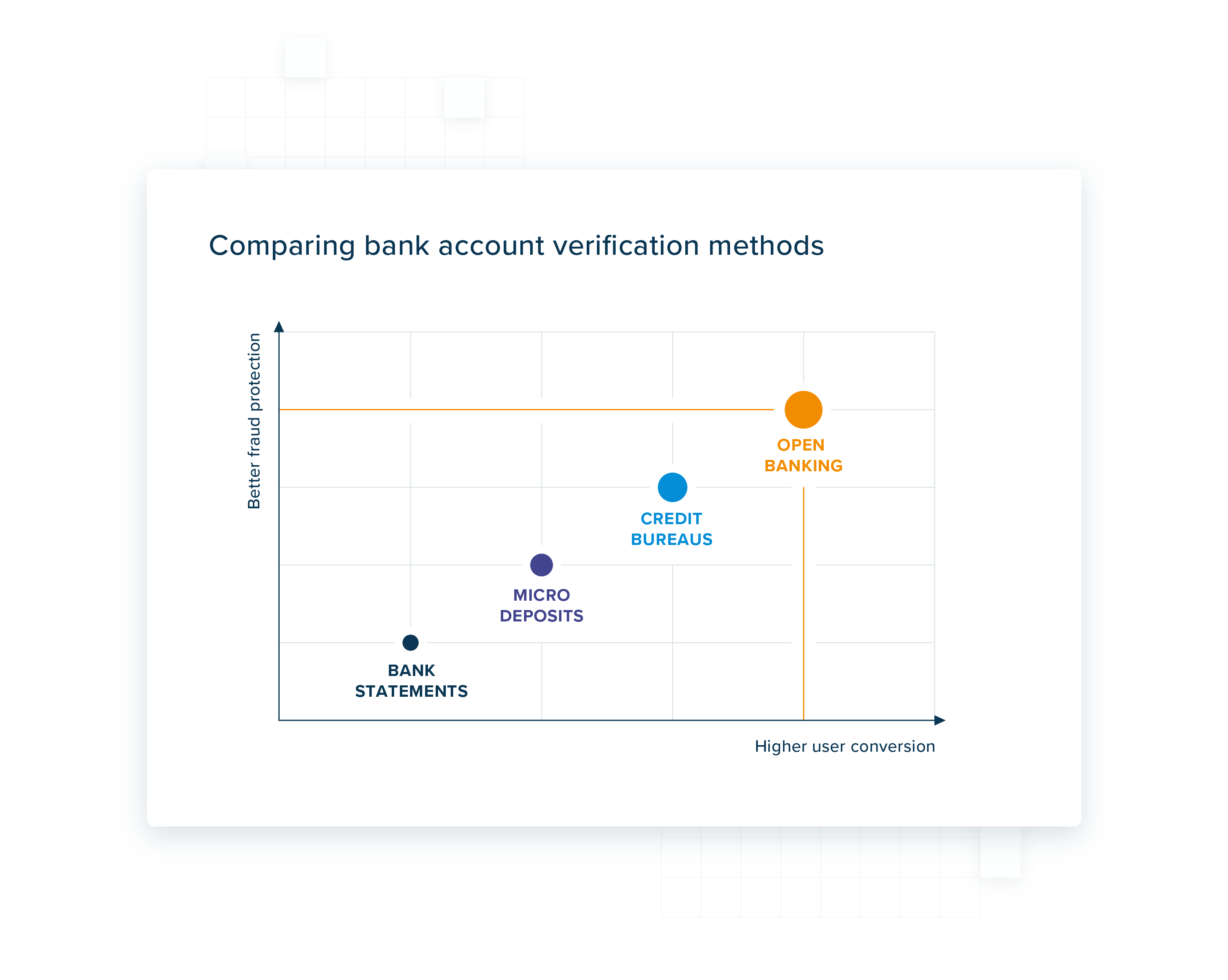

Limitations of bank verification methods

Manual bank account verification methods suffer from severe limitations, including security risks and low conversion. Considering the whole point of bank account verification is to reduce error, it’s surprising that many methods are vulnerable to mistakes on the customer’s end.

Micro deposits are a prime example. They only determine whether an account can accept payments rather than verifying a customer. This opens the door to errors, failed payments and even fraud. Micro deposits also rely on customers providing correct details. If they make a mistake, the process could fail.

Sending bank statements is also prone to human error, but its limitations don’t end there. The process is slow, costly and resource-intensive. It also carries a high risk of fraud since bank statements are relatively easy to forge.

)

By comparison, credit checks are faster and boast a higher conversion rate. But they also have their fair share of drawbacks. For example, they can fail when credit bureaus have outdated information on file. When that happens, customers must undergo a manual verification process, which is expensive and time-consuming.

Luckily, businesses can overcome many of these obstacles by verifying account information with open banking. This involves working with a regulated company called a third party provider (TPP). TPPs like TrueLayer offer account information services (AIS), and can access customers’ bank account information through technology called application programming interfaces (APIs).

The TPP can then instantly confirm that the information a customer provides matches with the information at their bank. Not only does this happen instantly, but the data is also real-time accurate, ensuring that the check doesn’t fail. Effort on the customer’s part is minimal, and potential for most fraud is very low.

Bank account verification with TrueLayer

TrueLayer offers several options that pair bank account verification with Pay by bank — data-rich open banking payments that provide real-time confirmation and bank-grade authentication measures.

Take TrueLayer Verification. An add-on to open banking APIs like Pay by bank, it allows businesses to confirm account ownership quickly and seamlessly. Featuring its own name-matching engine, TrueLayer Verification saves companies the work of analysing raw data streams to validate their customers' bank account ownership. As a result, it’s an ideal tool for ensuring the source and destination of a payment.

But bank account verification doesn’t just happen during payments. Financial services firms, iGaming operators and even some online merchants need to perform verification checks as part of their onboarding processes. Providing a smooth, secure and efficient experience can be the difference between converting an active user and losing a prospect forever.

That’s where Signup+ can help. Combining account creation, verification and a first payment, it streamlines the onboarding process and automatically converts signups into active users. Using bank-sourced identity data, Signup+ verifies the customer’s bank account immediately, removing the need for additional onboarding steps. The result: KYC-compliant onboarding that’s both fast and secure.

Bank account verification is a great way to prevent fraud and human error, but not all methods are created equal. Open banking-based solutions from TrueLayer can help you protect your customers without compromising their experience.

Learn more about Signup+ to see how open banking can help you onboard customers quickly and securely.

)

TrueLayer part of FCA's Supercharged Sandbox to test agentic payments

)

Payment choice, not cards by default: the view on agentic payments

)