)

)

Last week the payments-sphere exploded following press reports that major UK banks were conspiring to set-up an alternative to Visa and Mastercard.

The report lacked nuance about what is actually happening. A company ‘DeliveryCo’ is being established under the National Payments Vision. But DeliveryCo’s task — rather than building an alternative scheme (let alone a card scheme) — is to deliver next generation retail payments infrastructure.

In the UK, unlike the EU, there are, as yet, no bank-led plans to build a new stand alone payment method, AKA a UK Wero.

To be clear, we don’t need another Wero. We already have the foundations for an alternative to cards: Pay by Bank.

It’s a rapidly growing payment method, led by homegrown UK fintechs, modern API technology and is already live with some of the worlds largest merchants: eBay, Amazon, Ryanair.

But just as high speed trains need high speed rails, we do need better retail payments infrastructure, for Pay By Bank to deliver its full benefits for UK consumers and businesses.

Looking for something we can rely on

First thing’s first, why all the talk of alternatives to Visa and Mastercard?

Long before geopolitics ramped up concerns about over reliance on US-based card schemes, there were concerns about a lack of competition and crucially, payment resilience, both of which have direct costs to UK GDP.

Today, the UK payments landscape is heavily concentrated. Visa and Mastercard account for approximately 99% of UK card payments and 84% of all UK retail payments. This lack of competition is costing UK businesses an extra £170 million per year.

Beyond direct cost, this also represents a resilience risk. Payments system outages, temporary or otherwise, are no longer ‘black swan events’. The average UK business now reports more than five major outages a year, resulting in financial consequences:

£1.6bn in annual sales are at risk across the UK retail, hospitality and leisure industries due to payment disruptions.

Even short-lived failure can cost businesses significantly, with research suggesting that just 22 minutes of downtime can put over £1 billion in revenue at risk as customers quickly abandon their purchases. 22% of businesses have no backup method except cash.

The Government recognises these risks and work is well underway to support alternatives that sit alongside card payments, which fall under the umbrella of account to account payments.

HM Treasury’s National Payments Vision notes that “It is crucial that seamless account-to-account payments — enabling consumers to pay for goods and services in shops and online directly from their bank account — are developed’.

The Bank of England also recently said, “we want UK consumers to have the option to pay retailers in-store or online directly out of their bank accounts as a complement to doing so via card schemes”.

There's gotta be something better out there

The term account to account payment gives the impression of a consumer setting up a manual bank transfer from their current account, typing in sort codes and reference numbers, jumping in and out of apps. But there is already something better out there.

Since 2018, the UK has been leading the way in developing Pay by Bank. This uses open banking technology to enable a seamless way for consumers to pay merchants directly, and for merchants to accept account to account payments.

)

The open banking framework combines requirements on banks to support open, secure APIs, with a regulatory regime for payment initiators like TrueLayer, who connect into these APIs to enable merchant payment acceptance. In doing so, it drives fierce competition between fintechs, and rapid innovation.

A UK payments hero

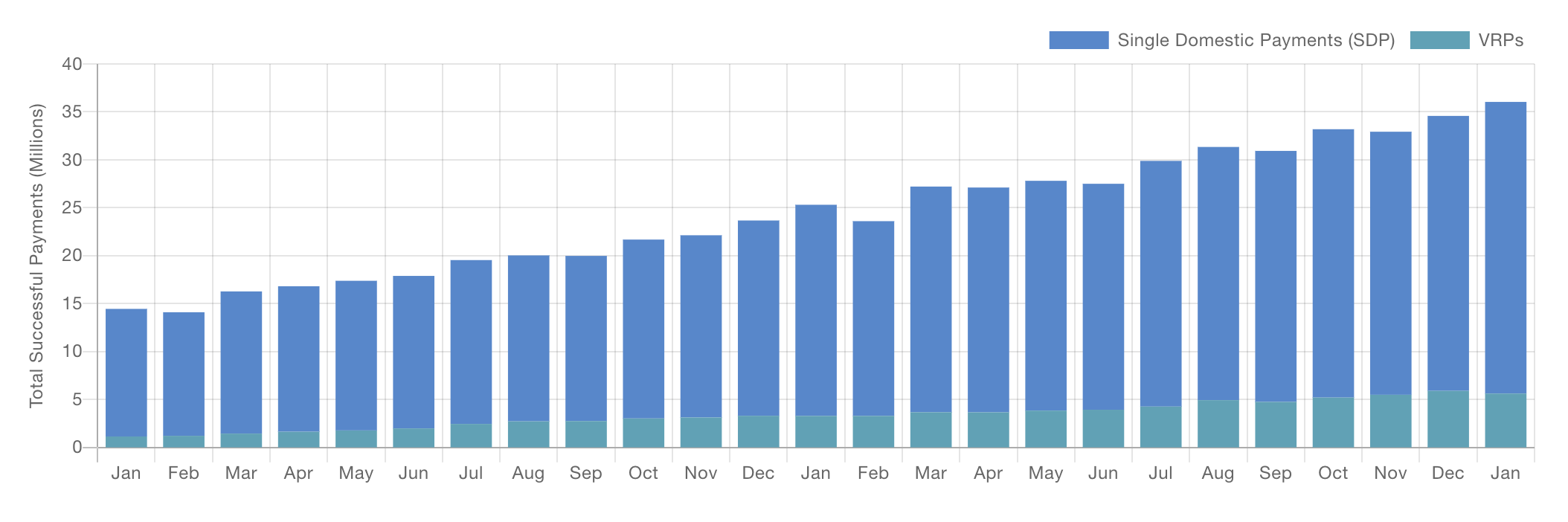

As a consequence, Pay by Bank is growing strongly (with 36 million transactions per month as of January 2026), and looks set to increase dramatically with household names such as Amazon, eBay, JustEat and Ryanair recently adopting the payment method.

)

Pay by Bank is a striking UK success story. A combination of regulatory initiative and fintech innovation. It provides the perfect foundation for the UK to build upon, to provide a truly ubiquitous alternative to cards.

But to fully deliver this resilience and competition, Pay by Bank needs to be enabled for in-store payments.

This can and should be achieved by building on Pay by Bank, rather than developing a new proprietary architecture or scheme, akin to a UK Wero. Starting from scratch, after banks spent £1.5 billion on open banking APIs, which successfully stimulated a strongly growing fintech ecosystem worth £4 billion, would be economically inefficient and lead to years of delay.

In our next article, we will unpack how the project to deliver next generation infrastructure, and the work to deliver new open banking payments functionality (the UK Payments Initiative) can converge to create a path to in-store Pay by Bank — capitalising on existing innovations, while delivering much needed competition and resilience at the check-out.

)

Bank on File is on the launch pad

)

TrueLayer appoints Stefano De Lollis as Head of Ecommerce

)