)

)

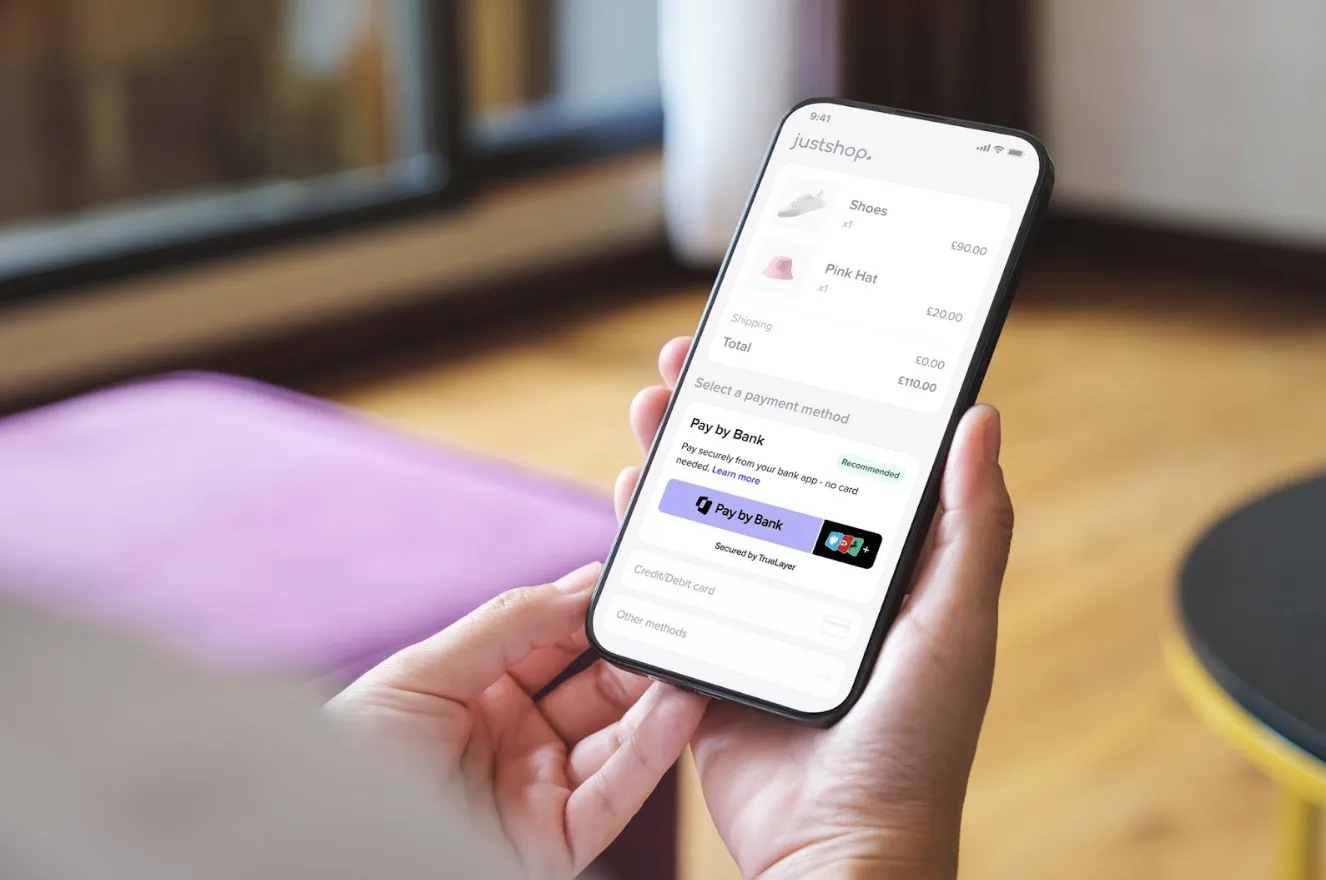

Pay by Bank is the fastest-growing payment method in the UK. It is already delivering benefits to millions of consumers and retailers.

Its success is aligned with Government and regulatory ambitions to create more payment choice, and reduce the cost of payments. It’s rapidly proving to be the most effective way of disrupting the card-scheme duopoly, whose dominance has resulted in UK businesses being overcharged and buried in complex, opaque pricing.

Pay by Bank eliminates the risk of card fraud, enables instant refunds, and gives retailers immediate access to funds — cutting out unnecessary intermediaries and dramatically reducing costs. That’s why millions of people use it every day, and why major retail brands are embracing it.

As we grow and enter new sectors, we’re constantly thinking about how to best meet the needs of consumers and businesses.

We designed Pay by Bank to be a safe, secure and efficient way to pay. Now we are focused on making sure it is the most convenient way to pay for goods and services of all types. We’re doing this by reducing the cost of payments with consumer incentives (coming soon); and we’re designing new protections for when consumers have purchase issues.

On protections, in recent months we have:

Undertaken a YouGov survey of 4,000 consumers on their use of and experience of refunds and chargebacks

Developed a blueprint for a new, efficient way to manage purchase issues, and merchant insolvency which we will test with merchants

Worked with banks and other fintechs on the options for additional protections in Pay by Bank

What are we solving?

In terms of consumer protection in Pay by Bank, there are three things to focus on:

Security: What happens if a payment is incorrect or unauthorised?

Insolvency: What happens if a business fails when you’ve paid in advance?

Disputes: What happens if a consumer and merchant disagree about a purchase?

Solutions

1. Security

The financial regulation that underpins Pay by Bank prioritises safety and security of payments. Pay by Bank does not involve sharing any card or security details online — so unauthorised transactions (where card details are stolen to make purchases), are a thing of the past — removing one of the primary reasons consumers use chargebacks. With Pay by Bank, if something goes wrong with your payment (such as the wrong amount is taken, or there's a duplicate payment), you have the exact same legal protections you have with any other payment option: you can get a refund from your bank.

2. Insolvency is being solved

TrueLayer primarily works with large enterprise merchants, so insolvency is a very low risk. However, as outlined in our 2025 Pay by Bank update, we are looking at ways to protect against merchant insolvency, to give consumers more trust and security against these rare events. We are exploring ways to add targeted protection for consumers, for edge-cases such as event cancellations. There are multiple ways to solve these issues, including looking at how liability is allocated and what combination of strategies such as merchant vetting, holding funds, or insurance can be used with Pay by Bank. The solutions we’re focusing on now are those that can add protection, without adding friction or cost to merchants or consumers.

3. Disputes need smart, modern processes — not outdated chargebacks

Businesses and consumers both struggle with card chargebacks: the complexity, the high costs, the slow processes and the refund fraud they enable (research shows that 48% of adults believe it is ‘reasonable’ to commit refund fraud). As a result, refund fraud is estimated to account for 60-80% of all chargebacks, adding £128m in costs for UK merchants, which are then passed back to honest consumers. The chargeback system, therefore, is not fit for purpose and has no right to be part of the conversation when we talk about purchase protection for Pay by Bank. We can, and will, do better.

Our blueprint explores how technology can help consumers who aren’t able to resolve an issue directly with a seller, and the role a central dispute resolution process can play, enabled by modern technology. We will do this without recreating the complexity or cost of the card scheme chargeback system.

An approach like this will offer consumers greater confidence and trust, without undermining the simplicity and efficiency that merchants and consumers love about Pay by Bank.

Next Steps

This work will inform the new central scheme for Pay by Bank: The UK Payments Initiative has now been established with the backing of the Financial Conduct Authority and will formally launch later this year. This is a cohort of 32 banks and fintechs who will agree on a set of rules and operating principles for Pay by Bank, Bank on file, and other open banking features. Together, we will drive Pay by Bank forward to make it a ubiquitous payment method as outlined in the government's national payment vision.

In the meantime, we will be publishing the results of our research and details of our blueprint and testing, to inform thinking and further progress.

)

TrueLayer appoints Stefano De Lollis as Head of Ecommerce

)

The 5 biggest benefits of Pay by Bank for consumers

)